Learn PPA Valuation For Financial Analysts

PPA Meaning in Valuation: Understanding Purchase Price Allocation and Its Role in Financial Analysis

Introduction to Learn PPA Valuation For Financial Analysts

PPA is another term that can be often met in the context of valuation and financial reporting when referring to mergers and acquisitions. The meaning of PPA in valuation is crucial to the finance professionals, valuers, auditors, and corporate decision-makers because it has a direct impact on the representation of acquisitions in financial statements and the evaluation of post-acquisition performance. Valuation and PPA are interconnected since the methods of valuation are the basis of assigning purchase consideration to identifiable assets and liabilities.

The paper describes the PPA full form in valuation, the idea of valuation of PPA and why PPA is an essential bridge between deal pricing, accounting standards, and long-term values measurement.

PPA Full Form in Valuation and Its Core Concept

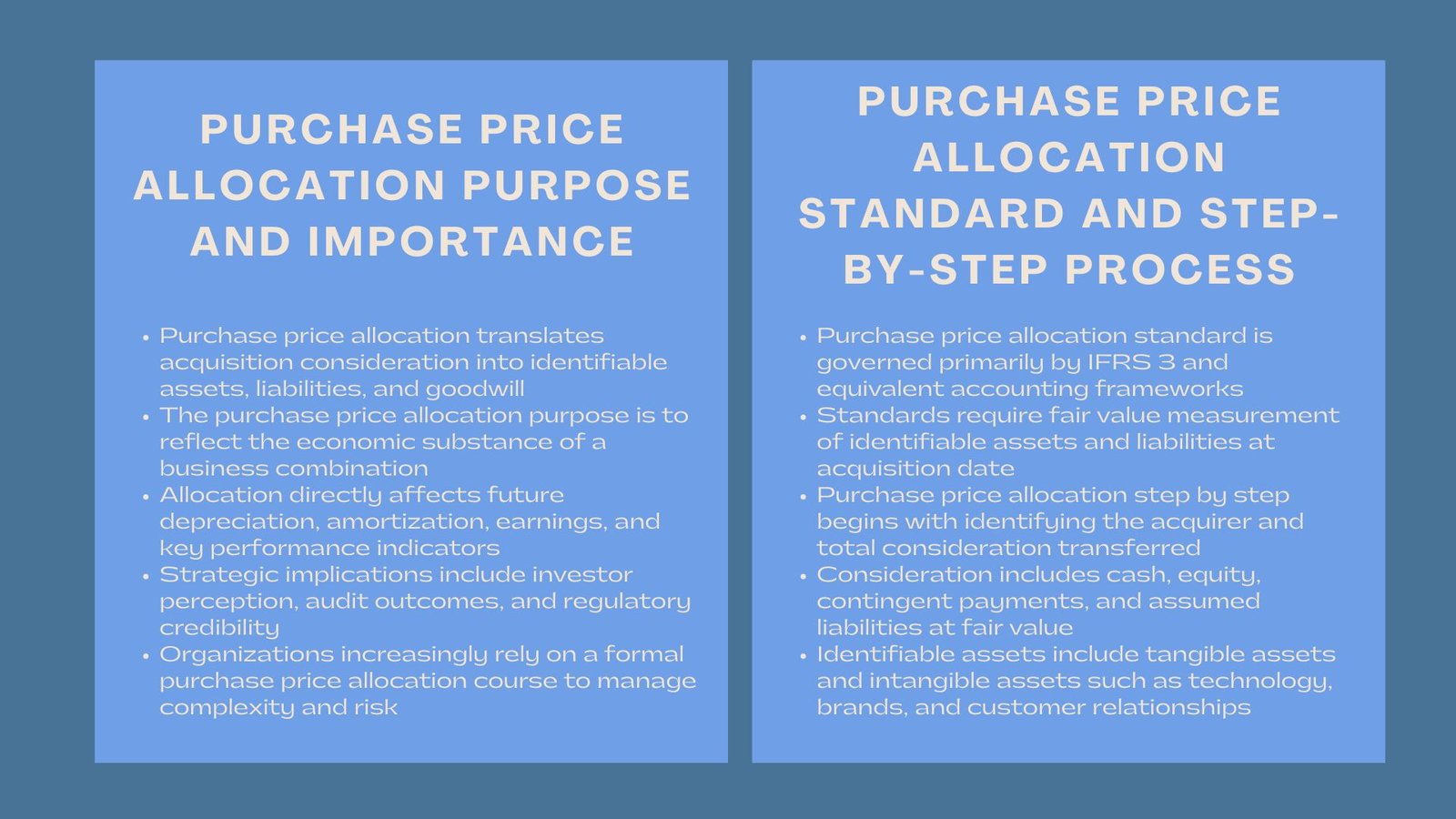

Purchase Price Allocation is the PPA full form in valuation. Purchase Price Allocation refers to the procedure of allocating the total amount paid in a business union to identifiable assets obtained and liabilities taken over at fair values on the date of acquisition. Any remaining balance on this allocation is classified as goodwill.

PPA is not an accounting process as far as valuation is concerned. It involves strict use of valuation principles in arriving at a fair value of tangible assets, identifiable intangible assets and assumed liabilities. This allocation would impact future periods of depreciation testing, amortization, impairment testing and reported profitability.

PPA Meaning in Valuation Practice

The meaning of PPA in the valuation extends past the accounting requirements of either the IFRS 3 or ASC 805. Practically, PPA is a systematic process of valuing that decomposes the price of transactions into asset values that are economically significant. This is done to ensure that the price of an acquisition is broken down into elements which indicates the driving forces of value.

Valuers undertaking PPA have to appraise customer relationship, brands, technology, contracts, licenses, and other intangible assets as to income, market, or cost approach. The resulting values do not only impact the financial reporting but also the internal performance measurements as well as the strategic decision-making.

Relationship Between Deal Value and PPA Valuation Outcomes

The point of PPA meaning that is most critically overlooked in valuation yet which has a direct correlation to valuation outcomes is the outcome of the purchase price allocation based on the negotiated deal value. Whilst transaction price depicts strategic considerations, market competition and the anticipated synergies, PPA valuation converts the negotiated price to quantifiable asset value based on fair value principles. Causes of inconsistencies PPP It can result in a mismatch between deal pricing assumptions and PPA valuation inputs that impacts on financial reporting credibility.

Practically speaking, valuation and PPA dictate the need to reconcile the acquisition premium and identifiable economic benefits. In the event that the actual purchase price is much higher than the fair value of identifiable net assets, then the good will grows. This is not to be mispriced, however it is to be heavily valued with robust reasons on why they expect to gain in the future using the economy. This reconciliation is frequently examined by analysts and auditors to determine whether goodwill is a reflective of sustainable value creation or a hyper-optimistic assumption in the deal structure.

Valuation of PPA and Fair Value Measurement

PPA is measured based on fair value measurement standards. Fair value is the amount that one receives in order to sell an asset or pay to transfer a liability in a market transaction to order participants. This in a PPA context will necessitate market based assumptions as opposed to entity based ones.

The multi-period excess earnings method, relief-from-royalty method, the multi-period excess earnings method, and the discounted cash flow analysis are the commonly utilized income-based techniques in valuation of PPA especially on intangible assets. The techniques depend on forecast, discount rates and useful life projections and hence professional judgment and valuation skills are very essential.

Valuation and PPA in Financial Reporting and Analysis

The centrality of valuation and PPA in post-acquisition financial reporting is a central concept of the relationship. After the purchase price allocation has been made the values of the recognized assets determine the future amortization and depreciation costs, which in turn directly impact the earnings and other financial ratios.

Moreover, the level of goodwill realized by way of PPA is liable to a test of impairment each year. Hyped or de-hyped PPA can thus contribute to misrepresenting financial outcomes, the economic performance and heighten the potential of future write-downs.

To investors and analysts, it is important to know how valuation assumptions are used in PPA during company comparisons, and in the success of acquisitions and the returns on invested capital.

Common Challenges and Judgement Areas in PPA Valuation

The pricing of PPA has several judgment-related aspects that contribute significantly to results. Identifying and isolating the intangible assets that were earlier not listed in the balance sheet of the acquirer is one of the most difficult. Customer relationships, proprietary technology, non-contractual customer lists and internally developed brands often necessitate valuation models created using paucity of observable market data.

The other issue is estimating the useful lives and the pattern of attrition of intangible assets. These assumptions would have a direct influence on amortization profiles and long term earnings. The presence of inconsistent or aggressive assumptions can cause distorted measures of the post-acquisition performance. Consequently, valuation and PPA require a disciplined response balancing economic realism and adherence to the principles of fair value measurement with the help of good documentation and sensitivity analysis.

Strategic Importance of PPA in Valuation Work

In addition to being compliance-related, PPA is strategic in terms of valuation and corporate finance. A properly implemented PPA gives one an idea of what an acquirer in reality acquired; it could be growth opportunities, intellectual property, customer relations, or synergies. It also assists in alignment of deal valuation and integration planning as well as creating long-term values.

When it comes to cross-border acquisitions or regulated industries, valuation and PPA are even more important, as there is a difference in accounting frameworks, taxation, and regulatory oversight.

PPA Valuation as a Tool for Post-Acquisition Performance Assessment

In addition to initial financial reporting, the definition of PPA in valuation goes further and to the post-acquisition performance analysis. Values that have been allocated in the purchase price allocation are considered as reference points with which the management assesses the success of integration, and asset performance. Amortization costs that are based on PPA affect the adjustments of EBITDA and operating margin and return measures that are applied by management and investors.

Also, the impairment testing depends on the initial PPA assumptions to a great extent. In case the projections of cash flows are not realized, the already identified goodwill and intangible assets may be subject to write-downs. Valuation and PPA are therefore not just accounting practices but are forward-looking tools which influence internal performance evaluation, capital allocation decisions as well as investor communication.

Conclusion

Overall, the PPA meaning in valuation has to do with applying valuation principles in the allocation of the purchase price in an acquisition to identifiable assets and liabilities at fair value. Purchase Price Allocation abbreviated as PPA in valuation is a crucial connection between pricing deals, accounting standards, and transparency of finances.

PPA valuation represents a technical art that needs valuation skills, judgment, and understanding of assumptions of the market participants. Finally, good understanding of valuation and PPA helps organizations to generate sound financial reporting, increase stakeholder confidence and make superior informed strategic decisions in the aftermath of business combinations.