PPA Best Practices for SMEs &

Professional Services in Singapore

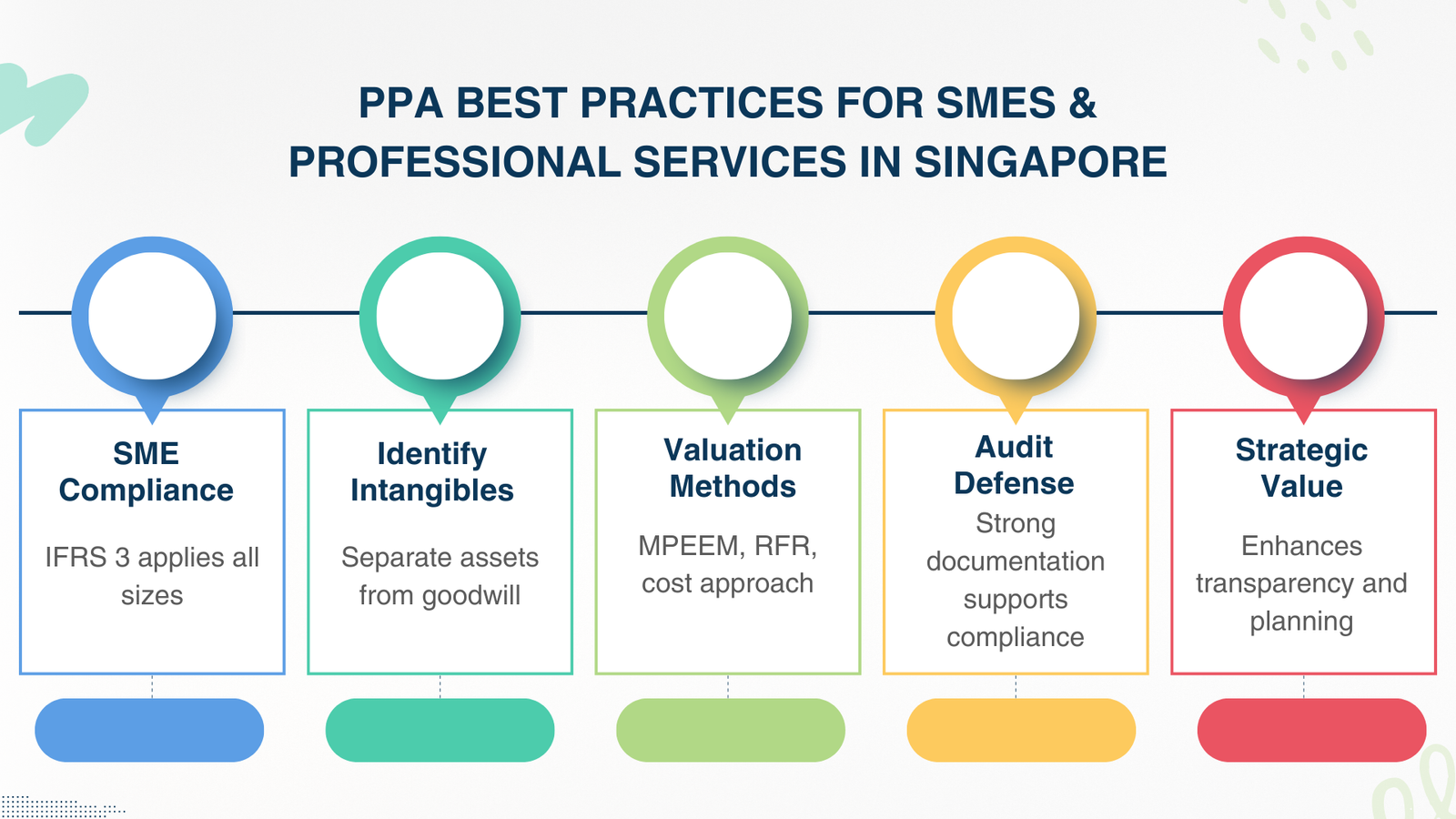

Introduction to PPA Professional Services in Singapore

PPA is Still Necessary to SMEs and Service Acquisitions

The widespread belief of both small and medium-sized business (SME) proprietors and their advisors is that Purchase Price Allocation Singapore is an issue of large scale dealings the territory of multinational corporations and investment banks. As a matter of fact, all business combinations, irrespective of the size of the deal, initiate the same accounting requirements. Whatever the case may be whether a Singapore businessman buys a neighbourhood dental clinic at S$800,000 or buys a mid-sized law firm at S$15 million, the acquiring company has to apportion the purchase price between the fair values of all identifiable assets and liabilities assumed.

Intangible assets often constitute most business value in SMEs that work within Singapore in the bustling services sector, both in the form of stores and food and beverage establishments and in professional service businesses developing law, accountancy and financial advisory services. The true economical resources are customer relationships, brand reputation, proprietary processes and expertise of the staff, although they have never shown up on a balance sheet. Failure to recognize and appreciate such assets appropriately disturbs the financial reports of the acquirer at the very outset posing compliance risk and distorting post-acquisition planning.

Besides, with Singapore still trying to make its mark as a regional professional services and SME financing centre, lenders, investors and the Accounting and Corporate Regulatory Authority (ACRA) are increasingly trying to see financial statements showing the actual economics of the transaction in the acquisition, irrespective of the scale of the transaction.

General Requirement of IFRS 3 Requirement Singapore Even on Small Business Deals

INEV Business Combinations IFRS 3 Requirement Singapore Business Combinations, which is applied in Singapore under SFRS(I) 3 in listed and public-interest entities, and to a large extent in Singapore Financial Reporting Standards to private businesses, requires all business combinations to be acquired. There is no size exemption. The standard sets that the acquirer identifies and measures all identifiable assets acquired, liabilities assumed and any non-controlling interest to their fair values at the acquisition-date.

In the case of SMEs which use full SFRS(I), Purchase Price Allocation Singapore Requirements are the same as those experienced by listed companies. Some requirements of the private companies that use SFRS can be simplified, but the principles of recognition and measurement, such as the need to disclose intangibles separately and to measure them at fair value, are substantively similar.

Learning about PPA of Retail and Service Businesses

Practical Case Study Sector Insights

In order to understand the essence of a reason that Purchase Price Allocation is relevant to SMEs and professional services firms, one may consider the following cases that are typical in the Singapore market:

Retail acquisition: This is where a retailer in the consumer electronics market acquires rival chain of seven outlets. Besides fitting and stocking of the stores, the purchase entails an established brand name, loyalty programme with 120,000 active members and preferred long term lease. All these are identifiable intangible assets or favourable contract positions that should be recognised and valued without consideration of the goodwill.

F&B business purchase: This is when a restaurant group buys an established hawker-turned-casual-dining brand. Intangible value drivers are the brand name, proprietary recipes (where legally protectable) and the trained staff. These assets fail to create real value because they are debilitated into amorphous goodwill without enhanced PPA.

Financial advisory company: This is a wealth management company that purchases a smaller financial adviser (FA) firm. The client portfolios, regulatory licences and trust relationships that are handled by the advisers of the acquired firm are the most valuable assets of the firm and are not reflected in the balance sheet of the acquired company at fair value.

Merger of law firms: A merger between a full-service and a boutique litigation firm. There is economic value attached to client mandate and continuing retainer relationship as well as reputational equity of named partners, which have to be factored in the PPA process.

Intangibles that are widespread in these industries

In all retail, F&B, professional services, and financial advisory, the most common types of intangibles to come across in a Purchase Price Allocation Singapore exercise are the following:

Brand equity and trade names: Established names have the advantage of customer recognition and premiums on customer loyalty especially in the competitive retail and F&B market in Singapore.

Customer lists and relationships: Economic relationships that lead to repeat revenues, but are not contractual, such as those in advisory, healthcare, and retail business.

Favourable contracts and licences: Low-market leases, favourable supplier agreements, regulatory licences and exclusive distribution rights.

Assembled workforce: Assembly workforce: Even though not classified separately in accordance with IFRS 3 Requirement Singapore, the existence of a skilled and trained workforce would tend to add value to other intangibles or goodwill.

Technology and systems proprietary: POC systems, CRM databases, and proprietary software are becoming a common part of SME acquisitions in Singapore.

PPP Industry-Specific PPA

There is a Retail Purchase Allocations

The profile of PPA in the case of retail acquisitions in Singapore is unique. There are large tangible asset bases in physical retail businesses as leasehold improvements, shelving and fixtures, point-of-sale equipment, and inventory. The premium gained over and above the net tangible assets however is normally intangible like the location of the stores, the brand, customer loyalty programme and supplier relationship.

Under IFRS 3 Requirement Singapore, the acquirer has to determine whether each of these value drivers is a separately identifiable intangible asset or otherwise it should not be classified as such and should be included in goodwill. A loyalty programme database containing quantifiable customer attrition patterns, and attributable revenue streams will, by way of example, be treated like the intangible of customer relationship, which should be separately recognized. Conversely, goodwill between the general customer and walk-in footfall can be fair to stay as goodwill.

Improved IFRS 16 lease obligations also include retail PPAs. The lease liabilities should also be determined by the value of the remaining payments at the date of acquisition, which is calculated at the incremental borrowing rate of the acquirer – both introduction of technical complexity but also economically significant information that the business actually did not cost as much as before thought.

Professional Services and Financial Advisory (RIA) Firms

In the case of regulated financial advisory and investment management firms, or licensed financial advisers, in the context of the Financial Advisers Act of Singapore, and client relationships and assets under management (AUM), are usually the key drivers of value.

The client relationship intangible in a Purchase Price Allocation Singapore of such firms is determined using Multi-Period Excess Earnings Method (MPEEM) which includes client attrition rates, revenue per client, operating costs and contributory asset charges. The crucial assumption is the retention rate of the clients: a company where relationship stickiness is high and there is a long period to relationships would be valued by the client relationship much high as compared to a company with high annual rates.

Also identifiable intangible assets may be regulatory licences, e.g. Capital Markets Services (CMS) licences or Financial Adviser (FA) licences issued by the Monetary Authority of Singapore (MAS): they may be transferable, and standalone in economic terms. Practitioners should determine whether the licence is entity-based or person-based since the person-based licences are not normally recognized to satisfy the criteria of IFRS 3.

Law Firms: Portfolios and Specialist Expertise of Partners

The combinations of law firms pose some of the most discerning Purchase Price Allocation issues in Singapore. In contrast to product firms, the intangibles of law firms hold almost all of their value: client mandates, reputation of practice area, partner relationships, and institutional knowledge.

Client portfolios – especially continuing retainer arrangement and multi-year advisory mandate could satisfy the contractual-legal requirement regarding separate recognition pursuant to IFRS 3. The non-contractual client relationships (e.g., clients who engage the firm on a matter-by-matter basis) can still be recognized under the separability criterion provided that they can be identified in the transactions involving similar lists of clients.

The expertise of partners and reputation are, however, inseparable as an intangible asset, but are intrinsic to the individuals, and not the company. The goodwill on the value of named partners is generally considered as a component of goodwill and the goodwill is also highly vulnerable to impairment when the significant partners leave after the acquisition has been made.

Determining Tangible and Intangible Assets

Physical Assets: Leasehold Improvements and Equipment

The most common element of a Purchase Price Allocation is tangible assets of SME and professional services acquisitions. They can be physical assets like office furniture, IT equipment, medical or laboratory equipment (in healthcare acquisitions) and leasehold improvements, motor vehicles, and inventories.

Tangible assets are usually valued by the use of the market method (references to second hand market prices of similar assets) or the cost method (replacement cost less depreciation). The independent property valuers and equipment appraisers are often utilized in Singapore to estimate the fair value in a credible manner especially regarding the fit-out improvements in a premium retail or medical premises.

Non-physical Assets: Brand, Contracts, Technology and Goodwill

In the majority of the SME and professional services acquisition, intangible assets are the largest part of the purchase price. In the context of IFRS 3 Requirement Singapore, intangible assets should be recognised independent of goodwill provided that they are identifiable that is, they fulfil either contractual-legal or separability test.

The main intangible categories to be taken into consideration are:

Brand value: This incorporates trade names, logos and other related consumer recognition. Valued on the principle of relief-from-royalty, with reference to observable rates of royalty in the market.

Customer relationships and customer contracts: Repeat sources of revenue and current customer bases. Priced on MPEEM or excess earnings basis.

Technology and software solutions: Applications, databases, custom systems and online tools. Being valued per relief-from-royalty or cost-to-recreate methodology.

Non-compete agreements: This is an agreement that limits the ability of sellers to compete with the new owner after the deal. The with-and-without method was used to value it.

Goodwill: This is the remaining amount of all identifiable tangible and intangible assets and liabilities that are not measured by fair value. Goodwill under IFRS 3 Requirement Singapore is not amortised, whereas, under IAS 36, undergoes testing on impairment periodically in a year.

One of the PPA pitfalls when conducting transactions in SMEs is the failure to distinguish the intangible assets by treating the whole premium as goodwill. This is not acceptable to the Purchase Price Allocation Requirements of IFRS 3 and will most probably be questioned by auditors.

Usual SME valuation techniques.

Market Approach

In the market approach, an asset or a business is valued based on the prices that have been paid on similar assets or businesses that have been transacted. In the case of SME PPA, the method is most suitable when it is possible to know the value of trade names or customer databases that have market royalty rates or multiples of transactions.

The market method is widely used in Singapore both to obtain brand value (based on industry royalty rate databases like RoyaltyRange or ktMINE) and as a benchmark of goodwill multiples to the prices of similar deals in the industry. The difficulty lies in identification of really similar transactions especially in the niche service industries where data on deals is minimal.

Income Approach: MPEEM and Relief-from-Royalty

The income method also measures an intangible in terms of future economic utility that it is likely to produce. Purchase Price Allocation Singapore exercises of SMEs are undertaken through two major approaches based on income:

Multi-Period Excess Earnings Method (MPEEM): The desirable method of customer relations and other key revenue generating intangibles. MPEEM separates those cash flows that can be ascribed to the individual intangible when returns on all other assets that contribute to it are subtracted. Some of the important inputs are revenue forecasts, client retention/ attrition, operating margins, and risk-adjusted discount rate.

Relief-from-Royalty Method: Assesses the value of intangible (a brand, technology, etc.) by saving on royalty by being able to own instead of license. The approach will need resultant royalty and revenue estimates. Auditors and tax authorities very much agree on the fact that it is based on observable market data.

Cost Approach

The cost approach calculates worth by looking at the amount that it costs to reproduce or replace the intangible asset and tries to adjust it by the obsolescence. It best fits proprietary technology, databases that have been assembled, and value involving workforce where there is little data on market or income.

In the case of SME acquisitions, cost method is usually the most viable way of valuing internally developed software or customised system especially when the acquiree has limited history of revenue or financial forecasts. It is also widely applicable in corroboration of income approach decisions of technology intangibles.

Detailed Strategy Value of PPA

Improved Planning of acquiring

A detailed Purchase Price Allocation Singapore is not simply a compliance requirement – it gives the acquirer a disaggregated picture of what was in fact purchased and at what price. This granularity can be useful in the decision-making process of a post-acquisition in a number of ways.

First, it also allows the management to monitor the performance of certain acquired assets. By valuing an intangible customer relationship at S$2 million based on the retention rate projection, the post-acquisition management will be in a position to measure the actual and projected retention against the modelling and take corrective action at an early stage in case the retention is running higher than modelled rates.

Second, it elucidates priorities of integration. Being aware of the fact that the brand is the key value driver, rather than the customer list or the technology will allow the management to spend resources to safeguard and capitalize on the asset. On the other hand, customer relationship should be regarded as the main intangible, which means that retention programmes and transition planning should be of higher priority.

Third, a properly implemented PPA will set a clean baseline on goodwill monitoring. When a large amount of the purchase price is still in the form of goodwill after an intensive intangible identification exercise, the management and auditors have more information regarding the nature and risk profile of the goodwill balance in the future.

True Amortisation and Deductions of taxes

Separately identified intangible assets Other than goodwill are amortised over estimated useful lives. In the IFRS 3 Requirement Singapore, a systemic amortisation is recorded in the income statement. In the case of SME, proper amortisation charges represent a better depiction of the quality of earnings and utilisation of acquired assets to the stakeholders.

In the Singapore tax context, inland Revenue Authority of Singapore is allowing capital allowance on select qualifying intellectual property and intangible assets under Section 14C, 19B, and provisions in the Income Tax Act. It may be possible to make legitimate claims of capital allowance with the help of a rigorous Purchase Price Allocation Singapore which identifies and values qualifying intangibles (in some cases, patents, licences and customer lists) which improves the after-tax cash flow of the acquirer during the amortisation period.

Nevertheless, accounting PPA and tax position need to be viewed as two independent concepts that should be aligned carefully. The difference between the two may raise the eyebrows of IRAS especially in the instances where capital allowances are claimed on intangibles that have received little value in the accounting PPA, or the other way round.

PPA Pitfalls to Avoid

Ignoring Intangible Assets

The most common PPA error made in the transactions of SMEs is the mere lack of identification and valuation of intangible assets. The entire purchase premium should not be treated as goodwill by the advisers (or by any acquirers who use their own assessment only) otherwise they have breached the Purchase Price Allocation Requirements of the IFRS 3 Requirement Singapore which expressly state that identifiable intangibles should be separately recognized.

Such an omission is most prevalent in SME transactions with involved advisers who are not experts at valuing intangibles, or in transactions where the acquirer and its accountants are concerned only with tangible assets and cash flows. The result is an exaggerated balance of goodwill that has no economic basis, imposes an impairment risk and could be a restatement should it be discovered by auditors.

Goodwill has been misclassified as Assets

Where the intangibles are determined, even, a related error is that of classifying certain identifiable intangibles to be goodwill. To take an example, an example of such a brand of cafe that obviously satisfies the separability requirement should not be included in goodwill just because it makes it difficult to value it separately. On the same note, the database of 50,000 members of the loyalty programme with their revenue attribution that could be measured should be measured as a potential list of customers intangible.

The practical effect of misclassification has two aspects: first the financial statements fail to reflect a true and fair view of what was acquired, and secondly, the charge of amortisation that would otherwise be recognised in respect of the intangible is never taken, inflating earnings in later periods until the goodwill is impaired in which case the charge is then recorded.

Inadequate Documentation

Even a technically sound Purchase Price Allocation lacks in having the ability to be defended. Poor documentation – i.e. lack of available valuation model, assumptions, or lack of evidence to support the choice of royalty rates – leaves the acquirer vulnerable to audit results, regulatory audit, and disagreements with IRAS. In Singapore, due to the high standards of professional accountability and a shift towards more attention on acquiring accounting quality, documentation standards are important.

It is best practice to prepare written PPA valuation report before finalisation of financial statements in the period of the acquisition. The report ought to record the scope of work, approach to be taken by the methodology to be used in each asset, major assumptions and explanation, and a reconciliation of consideration to values allocated.

Working With Auditors

The use of PPA Reports in supporting audit reviews

Auditors must under the Singapore Standards on Auditing (SSA) and the International Standards on Auditing (ISA) assess the compliance of the PPA of a client with IFRS 3 Requirement Singapore. In case of acquisitions of greater materiality, the auditor will normally examine the PPA more closely- determine that all identifiable intangibles have been taken into account, that methodologies to value intangibles are reasonable and whether important assumptions are evidenced.

A prepared and independent PPA report can contribute a lot to this process. It gives the auditor a clearly documented foundation on which the accounting has been made, minimizes the possibility of misunderstanding or contention, and shows the acquirer has taken its Purchase Price Allocation Requirements seriously. The precondition to clean audit opinion on an acquisition in many situations is the way of employing a qualified independent valuer instead of using internal estimates of the management.

In the case where the auditor has his own valuation specialists to review the PPA, the acquirer report is the major input to the review. An in-depth report that proactively responds to probable areas of challenge including the choice of royalty rate, assumptions about attrition, and derivation of the discount rate minimizes audit cycle time as well as a last-minute adjustment.

Meanwhile, Best Practices to Defend Assumptions

A number of practices can be used by SME acquirers to prove PPA assumptions to auditors:

Whenever possible, use observable market data: Royalty rates cited in third-party databases, attrition rates compared with industry research and discount rates based on capital asset pricing model (CAPM) models are all more justifiable than internal estimates.

Do sensitivity analysis: Indicating how the important value conclusions vary in the face of different circumstances, such as a 10 per cent change in attrition rate, or a 1 per cent change in discount rate, is indicative of analytical rigour and instills confidence in the auditor.

Reconcile to purchase agreement: This is to ensure that the PPA is based on the real terms of the acquisition and contingent consideration, working capital adjustments, and any representations and warranties which influence the value of the assets.

Start early: Starting the PPA process at an early stage means you do not have to work to meet audit deadlines and also there is time to refine the assumptions.

When to Recruit a Valuation Specialist

Complex Intangibles Valuation

Although the process of PPA can be conducted by a qualified CFO or external accountant on a number of grounds, some of the intangible assets may need the expertise of a specialist in valuation. In particular, when a qualified independent valuer is to be employed, the following items should be involved:

The acquisition entails big intangible assets and the value of these intangibles is substantial to the financial accounts.

Intangibles demand income-based methodologies like MPEEM which entails a complicated modelling of multi-period cash flows and contributory asset charges.

The acquiree is in a niche business such as financial services, technology or life sciences where sector standards and experiential learning are critical.

The overall consideration encompasses contingent or deferred elements (earn-outs) which in turn will have to be measured at fair value under IFRS 3.

The related party is the transaction, or it is of unusual structure and thus at risk of challenge by an auditor.

Audit Insurance and Reputational Insurance

Other than technical accuracy, independent valuation specialists offer credibility. An auditor who reviews a PPA which has been prepared wholly by management and has not been independently validated at all implements greater level of scepticism and could use his own specialists to conduct a counter-review. This adds to the cost of audit, prolongs the timelines, and exposes value revisions at the late part of the financial reporting cycle.

A PPA prepared by a recognised independent valuer, i.e. a Chartered Valuer and Appraiser (CVA), a member of the Royal Institution of Chartered Surveyors (RICS), or a charterholder of the CFA with appropriate experience has an intrinsic credibility. It is an indicator that auditors, investors, and regulators that the Purchase Price Allocation Singapore Requirements has been heeded and the financial statements can be trusted.

In the case of SMEs in Singapore looking to make acquisitions in the S$1 million to S$30 million sector or category, the cost of a professional PPA engagement is quite reasonable when compared to the size of the deal and is a sensible investment in financial reporting integrity and audit efficiency.

Conclusion

PPA as a Strategic and Compliance Tool

To the SMEs and the professional services firms in Singapore, Purchase Price Allocation does not represent any bureaucratic overhead, but rather a core instrument of coming to terms with, reporting, and managing the value created in the process of acquisition. Regardless of whether it is a retail brand acquisition, a financial advisory book of business acquisition, a portfolio of clients of a law firm, or a technology-enabled services business acquisition, one of the acquiring entities assumes a pre-established set of identifiable assets and liabilities the true value of which must be quantified and disclosed.

The existence of the Purchase Price Allocation Singapore Requirements of IFRS 3 is exactly to make sure that this measure is carried out strictly and publicly. In the case of acquirers who are thoughtful enough to identify all identifiable intangibles, use relevant valuation methodologies and ensure that their findings are documented then the exercise has enduring benefits: an effective asset registry, justifiable amortisation charges, justifiable goodwill balances, and a plausible post-acquisition performance management basis.

Enhancing Financial Reporting Integrity

Trust, transparency and professional standards are the pillars of confidence in the market of Singapore and this is where acquisition accounting has come under scrutiny. The emphasis of audit quality by ACRA, the reporting of disclosure carried out by the SGX on listed issuers, and the verification of taxes position of transactions by IRAS all fall on the PPA as a document of record.

The SMEs and professional services firms that invest in good Purchase Price Allocation Singapore practices through the support of independent valuation expertise and well-documented practices will be in a better position to not only meet the compliance requirement under the IFRS 3, they will also be in a better position to instill confidence in their investors, to finance further, and to show that they have done their acquisitions in a disciplined and careful manner.

Finally, a properly implemented PPA is a declaration on the quality of management. It states that the acquirer knows what it purchased, the price and the reason why it purchased it, and it is obligated to disclose that information with integrity.