Allocation of Acquisition Price in IT Services Companies

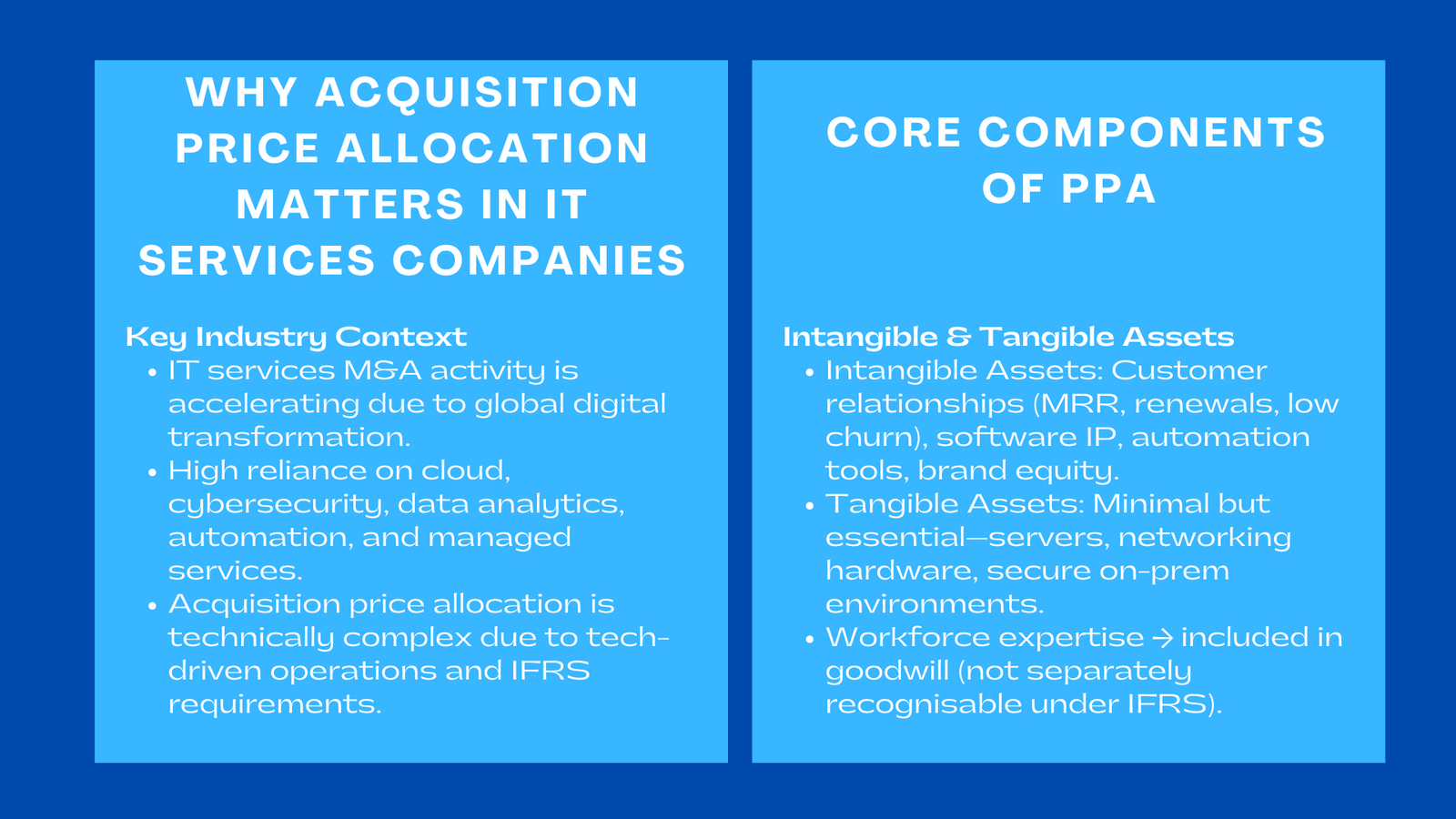

The IT services industry has become one of the busiest sectors for mergers and acquisitions as organizations around the world cut digital transformation efforts into overdrive. Companies of all sizes now rely heavily on cloud infrastructure, cybersecurity, software integration, data analytics, enterprise automation as well as managed IT support. This growing dependency has enhanced the strategic importance of IT service providers as well as fostering an environment in which acquisitions are not only frequent, but increasingly sophisticated as well. As a result, allocation of acquisition price in IT services companies has become a technically demanding process which requires a fine sense of technology driven operations, human assets, intangible value creation, and IFRS financial reporting requirements.

Unlike other businesses where physical assets contribute a significant share to the value of an enterprise, IT services purchase price allocation derive economic value from intangible resources such as software intellectual property, proprietary techniques, client relationships, service level commitments and the knowledge of specially trained teams. Because these value drivers are not directly reflected in the balance sheet itself, a properly conducted purchase price allocation (PPA) is needed to reflect transparently, in accordance with the regulations and to represent the business combination economically accurately. This process has gained special significance for technology SMEs for which recurring service models, long-term client engagements, and productivity frameworks with software are central to operations.

The valuation of IT service companies comes with special challenges since technology skills and intellectual capital are at the business model’s essence to drive revenue generation. Most acquired IT companies provide working through project based engagements, subscription service, cloud managed services, cyber security operations or service level arrangements (SLAs). Their capacity to develop revenue is determined by the technical know-how of their staff, the effectiveness of infrastructures within their business and the fidelity of their clients who depend on an effective and safe technology support. These characteristics mean that valuation analysts have to implement special methodologies for valuing the economic nature of technological services vs. traditional assets.

Furthermore, IT companies are in a landscape of innovation cycles. Technologies that are state-of-the-art when acquired may become obsolete in a short space of time if the company does not stay continuously innovating. Meanwhile, client expectations change rapidly, which forces providers to stay in accordance with industry norms, security systems, and digital transformation. These dynamics have implications not only for the fair value of intangible assets but also for the assumptions of goodwill, revenue forecasting and impairment testing.

For these reasons, the IT services purchase price allocation process demands extensive sector-specific knowledge, accountant treatment of operational scalability, consideration of technological relevancy and the discipline of applying IFRS reporting rules specific to technology-driven business models.

Understanding Purchase Price Allocation in IT Services Acquisitions

IFRS 3 and the Foundation of Asset Identification in Tech Companies

International Financial Reporting Standard (IFRS) 3 outlines the principles of business combinations that are used in accounting and the acquirer has to allocate the purchase consideration to identifiable assets and liabilities at their fair value. Because the IT services companies collect their value from their intangible sources, for the classification, measurement and recognition of these assets play a foundational role in the IFRS framework. The standard requires that intangible assets be recognised separately from goodwill where they are identifiable i.e. they emanate from contractual rights or are capable of being separated and transferred independently, which is why many practitioners refer to an IFRS 3 goodwill accounting and impairment testing guide Singapore when applying these requirements in practice.

In the context of technology SMEs, assets such as customer contracts, intellectual property, proprietary platforms, internal software tools, brand value and client relationships that are not covered by an individual contract often check these boxes. Many of these assets would not be captured in pre-acquisition financial statements since internally generated intangible assets are usually expensed instead of capitalized. However, under IFRS 3, they have to be brought on the balance sheet at the fair value on acquisition. This very often leads to a significant change in the structure of the post acquisition financial statements and involves careful valuation work.

The Nature of Economic Value in IT Services Companies

IT services companies enable value creation by combining a mix of human expertise and technological capability with long-term client relationships. They do not use it as their prime factor physical capital. Instead, value is imbued in the way we can provide consistent, secure and efficient services to multiple client environments. This involves technical skills, special instruments, methodologies, ways of sharing knowledge, etc. The workforce is central to success but IFRS does not allow workforce, assembled work force to be recognized as a separable intangible asset. As a result, the economic value of the expertise of personnel will usually be included in goodwill.

Meanwhile, intangible assets that can be identified (such as software IP, automation tools, operational frameworks and long-term client contractual relationships) need to be valued individually. This brings complexity as these assets tend to interact with one another and obtain value from network effects, combined use and integrated service provision. Financial analysts have to sort out these interactions and decide the fair value of each identified asset without losing the coherence with the enterprise’s valuation.

Core Components of Purchase Price Allocation in IT Services Companies

Tangible Assets: Operational Infrastructure Necessary for Technology Delivery

Although IT service companies do not have as many tangible assets as manufacturing or logistics businesses, there are still tangible items that are used to support important operations. These assets may range from an inclusion of server racks, networking equipment, specialist hardware used in testing environments, data storage devices, office infrastructure, and high-performance computing equipment used by technical personnel. Even for companies that are very cloud-driven, such as IT companies, they typically have hybrid setups in which their on-premise software hardware is necessary for secure operations, back-ups for data or any specialty work that is proprietary.

Tangible assets are usually just a small portion of the purchase price of an acquisition, but we know that they are crucial in allowing the provision of the service. Their fair value is based on market comparison, cost-based or replacement value analysis. Although these values are fairly easy to obtain, the correct recognition of these values ensures that the PPA process is complete and there is compliance with IFRS.

Intangible Assets: The Principal Foundation of IT Services Valuation

The intangible assets are the central value of most technology SMEs. Because IT services are based on intellectual capital, stable customer relationships and software-enabled efficiency, these intangible components are the backbone of the allocation of the purchase price.

Customer relationships are especially critical because IT service providers may have long standing service contracts, renewals and monthly recurring revenue (MRR) models with long-term customers due to managed service agreements, cloud support arrangements, cyber security monitoring or custom software maintenance. These relationships create predictable revenue streams with (in many cases) low churn, due to high switching costs faced by clients. Valuing of customer relationships Valuing customer relationships: to analyze relationship length between the contract, possible renewal of the contract, pricing stability of the contract, potential dependency to specific solutions, historical performance records of the customer.

Intellectual Property is another basic component of intangible value. This can involve proprietary software solutions, platforms, internal productivity tools, integration frameworks, automation scripts, cybersecurity monitoring systems or unique algorithmic processes. Even if these tools are not sold out but are used internally, it can materially increase the efficiency, lower the labor requirement or increase the quality of service, and this can affect the fair value. Under IFRS 3, such intellectual property needs to be recognised separately if they meet the criteria for identifiability.

Brand value also contributes to the intangible valuation, especially for the SMEs that have gained a reputation for reliability, technical expertise or special sectoral knowledge. A strong brand is useful in attracting enterprise clients, retaining existing customers and differentiating the company in crowded technology markets.

Technological know-how, training systems, and internal ways of service delivery have additional impacts on valuation. Although the assembled workforce cannot be identified as an intangible asset, the value arising from the staff expertise is included in the goodwill. Analysts must precisely tell the distinction between intangible assets recognized for separate recognition as well as expertise value in or in the form of goodwill.

Goodwill: The Residual Value of Innovation, Expertise, and Synergy

Goodwill, in the case of IT services acquisitions, is often very high as the value of intellectual capability, corporate culture, innovation capacity and un-identifiable competitive advantage holds significant value. Goodwill includes factors such as the reputation for good quality implementation, unbeatable responsiveness to clients, knowledge bank in the headquarter, and the synergistic cooperation to be expected by the integration of acquired business with a bigger platform.

Goodwill may account for expected growth from cross-selling opportunities, more expanded technological capabilities, higher cybersecurity offerings and better operations scale from integration of back-end systems. Due to the future impairment testing of goodwill, it has to be supported by reasonable assumptions and must be directly linked to identified cash-generating units.

External Factors Influencing Purchase Price Allocation

Technological Evolution and Its Impact on Asset Valuation

The pace with which technology is changing is one of the most important external influences on PPA of IT services companies. Tools and systems with high value at the time they are acquired may become useless if replaced by better working alternatives, or if client demands change to new technologies. Assessing the longevity, scale and competitive relevance of technological assets is therefore a crucial part in concluding what is fair value.

Different assets could have different economic lives depending on the industry sector in which the IT company is operating, e.g. cloud computing, cyber security, automation or enterprise software integration. Analysts have to assess whether technological assets continue to be economically viable over the valuation horizon.

Market Competitiveness and Client Retention Risks

IT service companies are in a very competitive environment. Market dynamics, price pressure, customer churn risk and overall repositioning of the competition all impact the assumptions sought in customer relationship valuation and goodwill estimation.

A company with defensible expertise, long client history, and good SLAs with specialized knowledge in a particular area may fetch a higher valuation due to the reduced client turnover risk on their service model. Conversely, the downward journey towards revenue adjustment in the PPA process may be experienced by firms operating in commoditized service markets.

Regulatory and Data Protection Considerations

Data protection regulations, cybersecurity frameworks, contractual obligations and compliance obligations have a significant impact on the IT company valuation. Firms with advanced security credentials or strong compliance systems are worth more because they lower the risk of reducing operational risk. Meanwhile, compliance gaps or antiquated data protection frameworks may mean valuation adjustments in companies with breaches may need to be made to reflect possible liabilities as well as risk-adjusted revenue projections.

Conclusion to Allocation of Acquisition Price in IT Services Companies

Purchase price allocation in IT services companies is a complex and strategically meaningful process which requires understanding of technological assets, client relationships, intellectual property, workforce capability and changing market. Since intangible assets comprise much of the value of technology SMEs, the division of acquisition price is an exercise combining financial valuation, technical judgment and regulatory expertise.

The well implemented PPA helps in making IFRS reporting tech SMEs, ensuring that the financial statements are accurate, and also allows the measurement of goodwill to be accurate. It gives an insight into the assets that really lead to profitability and future growth. As the pace of digital transformation and the importance of IT services to business operations continue to increase, the companies that are buying tech SMEs will continue to use rigorous processes for allocating purchase price as a guide for integration strategy, financial planning, investment analysis, and long-term competitive positioning.