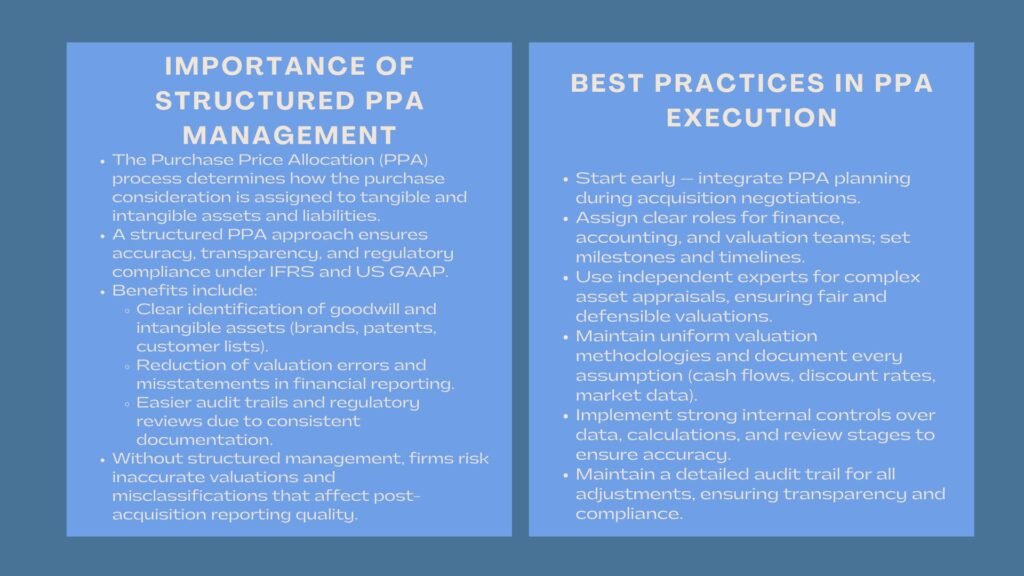

Best Practices for PPA Integration

Best Practices for Managing PPA Process and Integration After Acquisition Introduction to Best Practices for PPA Integration One of the most important processes of mergers and acquisitions is the management of the Purchase Price Allocation (PPA) procedure and the process of integrating an acquired company. The structured approach would also make sure that the determination […]

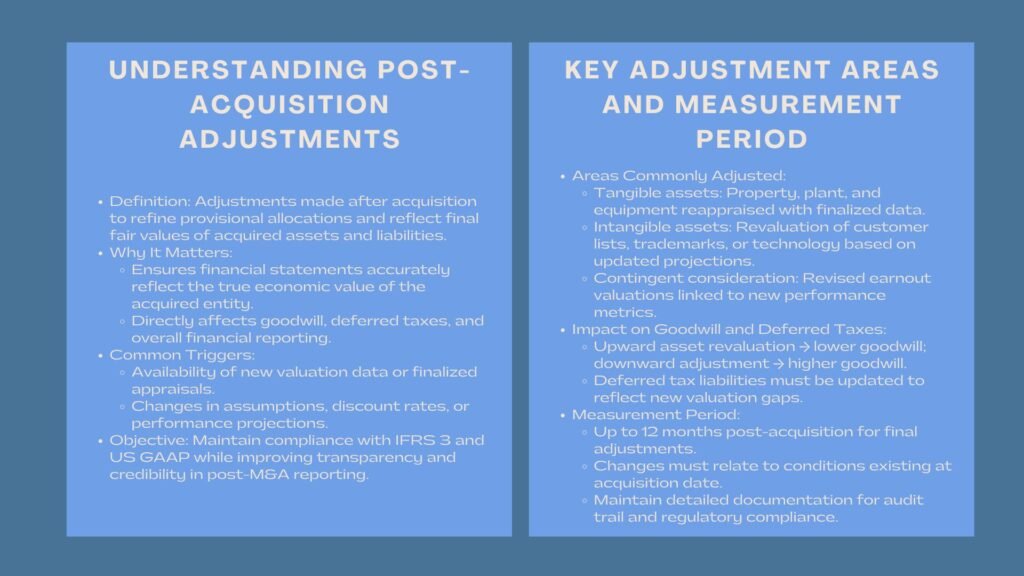

Certified Post-Acquisition Adjustments Training

Post-Acquisition Adjustments: Revisiting Purchase Price and Fair Value Changes Introduction to Certified Post-Acquisition Adjustments Training Acquisitions are not easy deals and even when the final price is set the finance department usually has to re-assess the original allocations to incorporate new facts or amend the tentative calculations. Adjustments made after the acquisition is a very […]

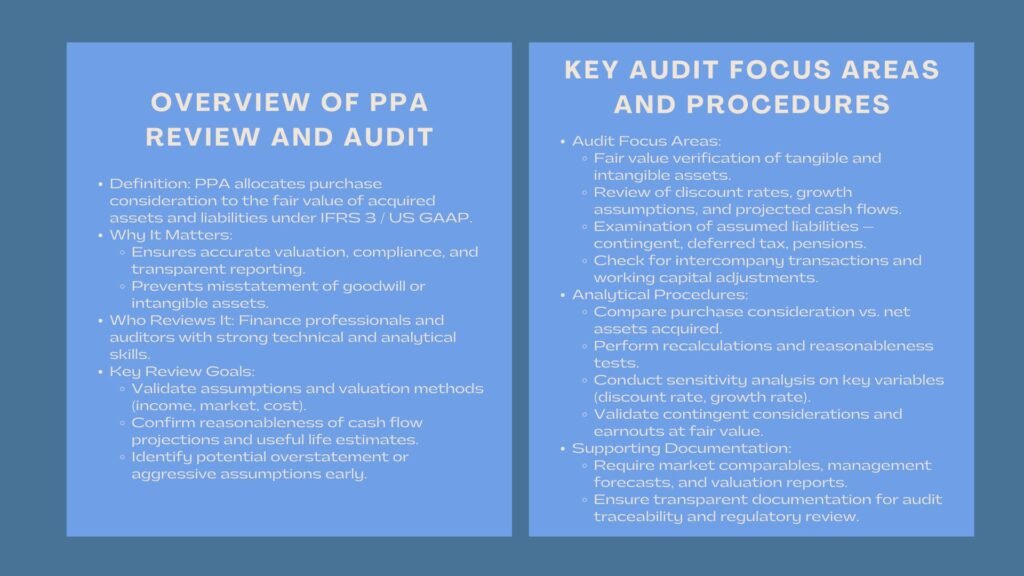

How to Review and Audit a PPA Report

How to Review and Audit a Purchase Price Allocation Report Introduction to How to Review and Audit a PPA Report One of the key elements of merger and acquisition accounting is purchase price Allocation (PPA), which is the allocation of the consideration of purchase to the fair value of the assets and liabilities acquired. Being […]

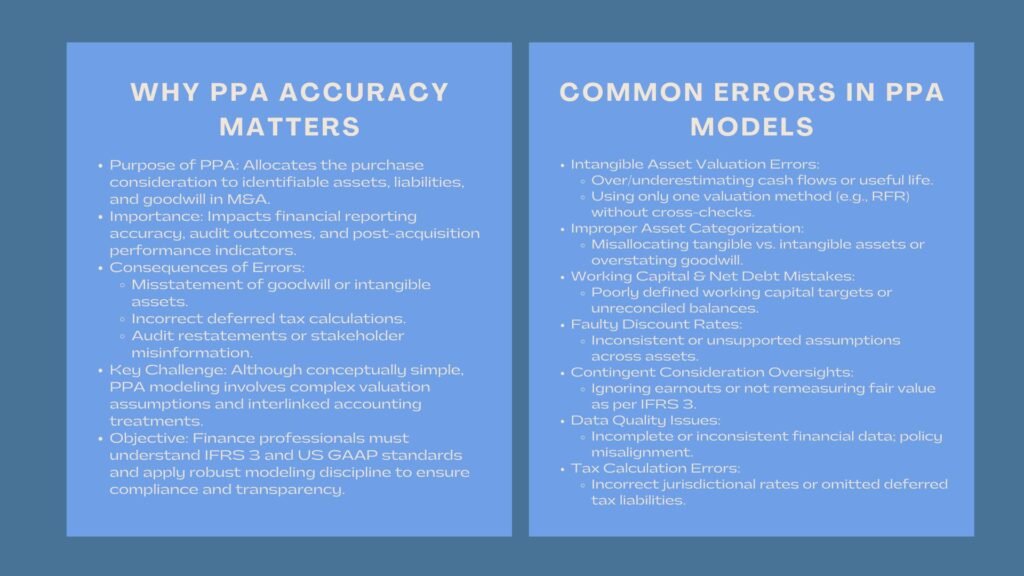

Certified PPA Modeling Error Analysis

Common Errors in PPA Models and How to Avoid Them Introduction to Certified PPA Modeling Error Analysis Purchase Price Allocation (PPA) is a very important procedure during mergers and acquisitions, under which the purchase consideration will be allocated to identifiable assets and liabilities, including intangible assets, and goodwill. Although the concept of the PPA modeling […]

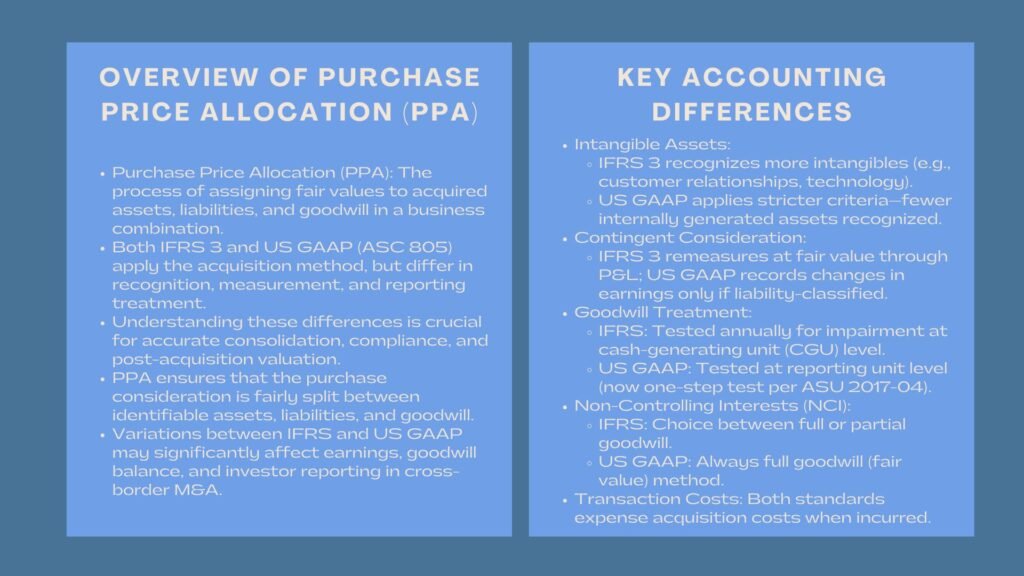

Certified IFRS 3 and US GAAP Course

IFRS 3 vs US GAAP: Key Differences in Purchase Price Allocation Introduction to Certified IFRS 3 and US GAAP Course One of the basic points of accounting business combinations is called Purchase Price Allocation (PPA). Both the IFRS 3 and US GAAP frameworks give guidelines on assigning the consideration to purchase of the acquired assets […]

Global IFRS 3 PPA Certification Program

Case Study: PPA for a Cross-Border Acquisition under IFRS 3 Introduction: Global IFRS 3 PPA Certification Program The complexities that are presented by cross-border acquisitions are beyond traditional PPA. The disparities in the accounting activities in the local areas, exchange rate, taxation systems, legal systems form hurdles in the establishment of reasonable values of such […]

Accredited Intangible Assets Valuation Course

Case Study: PPA for a Technology Start-Up with Intangible Assets Introduction: Accredited Intangible Assets Valuation Course The reason behind the uniqueness of technology start-ups as targets of acquisition is that they are highly dependent on intangible assets as opposed to physical property. In such situations Purchase Price Allocation (PPA) can be very instrumental in ensuring […]

Accredited IFRS 3 PPA Certification Program

Case Study: Purchase Price Allocation for a Manufacturing Company Acquisition Introduction: Accredited IFRS 3 PPA Certification Program The process of acquiring a manufacturing firm necessitates careful thought with regard to the arrangement of financial, operational, and strategic planning to make sure that the purchase process brings about value and adheres to the accounting and regulatory […]

Professional Tax Implications IFRS Certification

Tax Implications of Purchase Price Allocation and Consideration Adjustments Learn Professional Tax Implications IFRS Certification Purchase Price Allocation (PPA) of M&A transactions is not only the basis of accounting goodwill but also tax consequences are serious. Consideration alternatives, including contingent or deferred payments, have an impact on deductibility of expenses, recognition of deferred tax and […]

Certified IFRS 3 and IFRS 9 Valuation Course

Reassessment of Contingent Consideration: IFRS 3 and IFRS 9 Treatment Learn Certified IFRS 3 and IFRS 9 Valuation Course The aspect of contingent consideration frequently develops after an acquisition since the performance criteria are achieved or market conditions vary. The rules to follow in assessing are extensive in IFRS 3 and IFRS 9 depending upon […]