Financial Reporting Valuation Malaysia

A Practical Guide for Junior to Mid-Level Finance Professionals

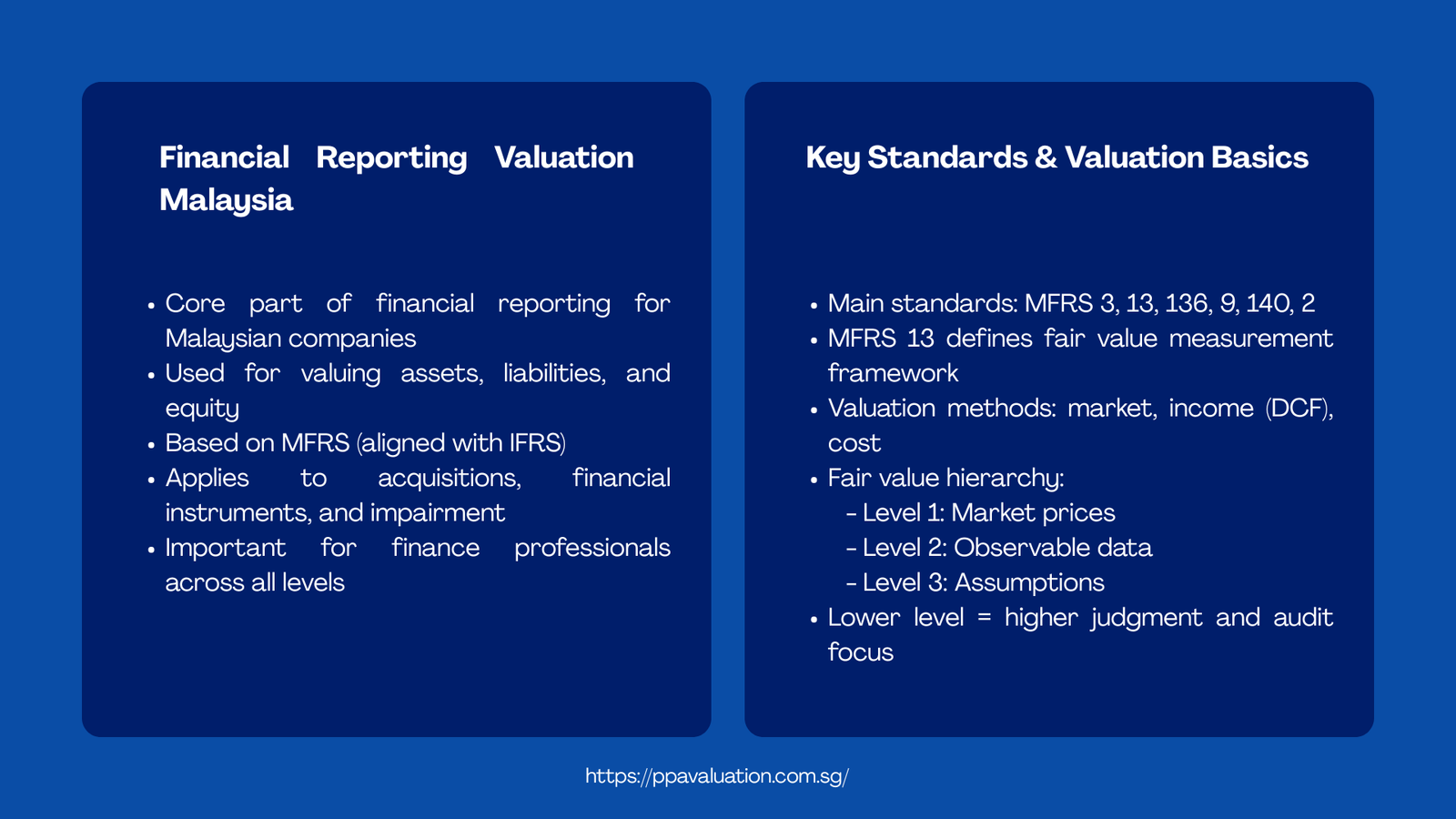

Introduction to Financial Reporting Valuation Malaysia

Financial Reporting Valuation is no longer a minor expertise that only deal teams or Big Four consultants know about; in the case of finance professionals in Malaysia. With an increase in the complexity of Malaysian companies expanding in terms of multiple industries, the acquisition of subsidiaries, or being listed on Bursa Malaysia, the need to have the correct and standards-conform valuation to the financial statements has increased tremendously.

Financial Reporting Valuation is, in a nutshell, the process of arriving at a fair value of assets, liabilities or equity instruments with a view to presenting and reporting financial statements in accordance to the applicable accounting standards. The Malaysian Financial Reporting Standards (MFRS) framework that is converged with International Financial Reporting Standards (IFRS) governs this in Malaysia. Valuation is at the crossroads of accounting, finance and economic analysis whether testing goodwill of a business combination, accounting financial instruments at fair value or impairing business combination.

The article is addressed to people, who enter or develop their career in the sphere of Malaysia Financial Valuation with fresh graduates, junior associates in valuation firms, finance executives in public-listed firms, and job seekers preparing to be in transaction advisory or technical accounting. It is aimed at providing you with a practical sense of how this discipline works, the most common assignments you may be involved in, and what problems you may expect to encounter on the ground.

The Standards That Drive Valuation Work in Malaysia | Financial Reporting Valuation Malaysia

The starting point for any MFRS Valuation Services engagement is the awareness of what accounting standard initiates the requirement. Financial reporting valuations are not like valuations that are primarily prepared because of tax purposes or purely transactional purposes, as they are subject to particular MFRS standards that dictate when fair value should be measured and how this measurement should be performed and what disclosures should be made. One can get the standard wrong at the start of it and nullify the whole approach.

The more common standards in practice are the MFRS 3 (Business Combinations) standard which requires the recognition and measurement of identifiable assets which have been acquired, liabilities incurred and any arising goodwill of an acquisition. MFRS 13 ( Fair Value Measurement) is the general umbrella framework, which states that fair value is determined as the amount that would be received in order to sell an asset, or paid in order to transfer a liability in an orderly transaction between market participants on the measurement date. MFRS 136 (Impairment of Assets), MFRS 116 (Property, Plant and Equipment), MFRS 140 (Investment Property), MFRS 2 (Share-Based Payment), and MFRS 9 (Financial Instruments) are some of the other standards that have been widely referred to.

The fair value hierarchy that categorizes inputs used in valuation into three levels is one of the main principles that have been enacted under MFRS 13. Level 1 quotes are quoted in the most active market – most trustworthy. Level 2 inputs can be seen but not quoted, e.g. similar transaction multiples or yield curves. Level 3s are the inputs that cannot be observed, which uses the assumptions of the entity, and which are the most widespread in the Malaysian practice due to the relative shallowness of some domestic markets. Knowledge of such a hierarchy assists professionals in communicating the validity of their conclusions and be ready to undergo audit oversight.

Table 1: Widespread Valuation Methods MFRS.

| Valuation Method | Applicable MFRS Standard | Common Use Case | Key Input Required |

| Market Approach | MFRS 13 | Listed securities, land | Market comparables |

| Income Approach (DCF) | MFRS 136 / MFRS 3 | Goodwill impairment, business combinations | Discount rate, cash flows |

| Cost Approach | MFRS 116 / MFRS 140 | Specialised assets, PPE | Replacement or depreciated cost |

| Option Pricing Model | MFRS 2 | Share-based compensation | Volatility, risk-free rate |

| Net Asset Value | MFRS 10 / MFRS 3 | Holding companies, M&A | Asset/liability fair values |

5 Key Steps in a Financial Reporting Valuation Engagement in Malaysia

Although each engagement is unique based on the type of asset and standard used, the majority of MFRS Valuation Services engagements have a uniform process. This knowledge of this workflow also assists in making junior professionals meaningful contributors that the organization can have before they are running projects on their own.

Defining of the scope and purpose is the first step. This implies the validation of the valuation topic, the applicable MFRS standard, the date of valuation and the purpose of the report. Valuation prepared under MFRS 3 purchase price allocation (PPA) appears very different with that prepared under MFRS 136 impairment testing, although the underlying asset may be the same. The second one is data gathering, which normally involves examination of audited financial accounts, management accounts, business plans, forecasts, and any other pertinent legal agreements. Management interviews are usually done to be familiar with the business model, competition and what is important in the business.

The third one is model building, which involves the valuer choosing the right methodology; the income approach, market approach, or cost approach and building the financial model. Professional judgment is applied the most here either the choice of discount rates, identification of similar companies, projection of useful economic life of intangible assets, or royalty rates in brand valuations. The fourth step is peer review and quality control, which is to make sure that the model is internally consistent, assumptions are supported, and conclusions are defendable. The fifth and last one is report writing and audit support, during which the findings are officially recorded and the valuation professionals collaborate with the auditors of the reporting entity in order to answer questions and complete disclosures.

Process Flow: 4 Step Valuation Workflow at a Glance

| STEP 1 | STEP 2 | STEP 3 | STEP 4 |

| Scope & Purpose | Data Gathering | Model Build & Review | Reporting & Sign-Off |

| Identify asset/liability. Confirm standard (MFRS 3, 13, 136, etc.) and valuation date. |

Get financial reports, projections, market information, invoicing history and contractual documents. |

Use approach (DCF / market / cost) of choice. Stress-test assumptions. Peer review model. | Issue valuation report. Coordinate with auditors. Complete financial statement disclosures. |

| Output Deliverable: letter, scope memo | Output Deliverable: Data checklist, management interviews. | Output Deliverable: Draft valuation model, sensitivity table. | Output Deliverable: Final report, audit support file |

Understanding Financial Reporting Valuation Malaysia Through Real-World Applications

To gain an appreciation of how Malaysia Financial Valuation is working in practice it is good to consider particular situations that are prevalent in domestic market. The purchase price allocation following a corporate acquisition is one of the situations that happen most of the time. Take the example of a Malaysian conglomerate which buys a logistical firm in the region. The acquirer should recognise and separately measure all identifiable intangible assets in accordance with MFRS 3 which includes customer relationships, technology platforms, and trade names at their fair values on the acquisition-date. The remaining sum that is paid over the net fair value of identifiable assets is then goodwill. This is a typical PPA exercise that many junior professionals get their first complex valuation engagement.

The other prevalent case is annual testing of impairment of goodwill, which is to be conducted by the public-listed companies in Malaysia under MFRS 136. This is normally a discounted cash flow (DCF) analysis of the cash-generating unit (CGU) that the goodwill allocation has been charged to. A manufacturing group that has operations in several segments e.g. would have to test the good-will in each CGU individually – using segment-based discount rates and growth assumptions that may be especially tricky in turbulent economic times. The COVID-19 experience showed a marked rise in impairment charges in the aviation, hospitality and retail sectors, which supports the direct flow of macroeconomic environment to Financial Reporting Valuation results.

Malaysian reporting is also characterized by property valuations of investment properties under MFRS 140. Real estate investment trusts are listed in Bursa Malaysia and are required to record their investment properties at fair value where their values change in the profit or loss. This normally involves involvement of registered valuers under the Valuers, Appraisers, Estate Agents and Property Managers Act 1981, though financial reporting valuers usually help in reviewing such values to meet MFRS requirements, especially where the property is still under development or there is any lease restructure.

Key Professional Lessons for Aspiring Valuation Professionals | Financial Reporting Valuation Malaysia

The availability of market data of some of the asset classes is also one of the most consistent problems of the Malaysian Financial Valuation. The capital market of Malaysia, though highly developed on the ASEAN level, is relatively concentrated, thus it is hard to find any sufficient listed comparables to the niche markets such as Islamic fintech, agri-processing, or industrial gases. Valuers frequently have to consider regional comparables of Indonesia, Thailand or India and make appropriate size, liquidity and country risk premium adjustments. The judgment necessary to arrive at such adjustments, and to record them, clearly, is a skill that good valuers have and average valuers do not.

The other issue that is recurrent is the management of the relationship between the auditors and the valuation team. In line with MFRS 13 and Malaysian Institute of Accountants (MIA) recommendations, auditors must take into consideration the reasonableness of noteworthy assumptions in the valuation made by management. This puts the valuation team in a situation where not only are they required to create technically sound work but they also need to foresee audit review and preemptively record the reasoning behind each of the major assumptions. The junior professionals must establish the habit of keeping clear audit trails in their models at an early age so as to record the origin of the input, the date when the input was obtained and adjustments done.

Another area that most professionals are not well prepared is the complexity of valuing intangible assets. There is no market value of intangibles like customer relationships, technology, brand names, and the analysis to value this intangible needs to be done analytically, through methods such as the Multi-Period Excess Earnings Method (MEEM) of customer relationships or by methods like the Relief-from-Royalty of brand values. Such methodologies must have a good understanding of both accounting and economics, and can be circular (e.g. when the value being computed to amortise a tax benefit is calculated by using another value itself, requiring a laziness in modelling). These skills are acquired over a long period of time, but by simply being exposed early in life on how these models are organized, your progress will be fast.

Table 2: Common pitfalls in Malaysian Financial Reporting Valuation

| Challenge | What It Looks Like in Practice | Practical Mitigation |

| Thin market data | Minor number of listed comparables in niche (e.g. healthcare REITs, plantation tech) | Adjust regionals using peers adjustment of size/liquidity. |

| Discount rate subjectivity | Assumptions on WACC are diverse particularly to unlisted entities. | Record all elements using third-party market data indicators. |

| Auditor vs valuer disconnect | The key assumptions are questioned by the auditors after submission which creates delays. | Engage the audit group; settle on the methodology before the fieldwork. |

| Currency & macro risk | The movement of ringgit influences fair value of the foreign-denominated assets. | Apply consistent FX rates; report currency sensitivity in notes. |

Skills and Career Growth in MFRS Valuation Services | Financial Reporting Valuation Malaysia

Malaysia is providing increasingly more entry points to those who are interested in starting a career with MFRS Valuation Services. All of the Big Four accounting firms (Deloitte, EY, KPMG, PwC) have valuation practices in Kuala Lumpur which operate on financial reporting, transaction advisory, and litigation support assignments. Boutique advisory firms, especially those specializing in mid-market M&A also are good sources of exposure to PPA and impairment work. The larger public-listed companies, which have corporate finance teams, are increasingly bringing valuation capabilities in-house, which puts pressure on the demand of a person that is able to do both the preparation and the audit defence of the financial reporting valuation.

On qualification factors, the ACCA qualification and the Chartered financial analyst (CFA) designation are well known and have excellent foundational knowledge in the valuation and financial reporting respectively. Individuals with a specific interest in the field of valuation can also look at the Chartered Business Valuator (CBV) designation, which is granted by the RICS on work of a property-related nature, or certifications offered by the American Society of Appraisers (ASA). What employers in this space are always after however is a blend of technical modelling skills, accounting literacy, and written communications skills – the skills to communicate difficult valuations to non-expert audiences clearly, such as audit committees and board members are highly prized.

An example of practical ideas related to the beginning of a career: offer to be in charge of a part of the valuation model, even as a support person. It may be the construction of the discount rate calculation, the filling of the similar-companies table or the writing of the methodology section of the report, but all that is done to accomplish these tasks is to construct a transferable skill. The more you know how each element will relate to the ultimate value conclusion the sooner you are going to emerge as a well-rounded Financial Reporting Valuation professional.

Conclusion: Key Recommendations for Next Steps

Financial Reporting Valuation in Malaysia is an arduous yet gratifying field that is at the centre of the financial reporting integrity. With the changing regulatory landscape as the regulatory surroundings are upgraded by Bursa Malaysia and the Securities Commission discussing the standards of further improvement of disclosures and audit work, the relevance of credible and well-documented work on valuation will receive even greater significance.

As a junior professional in this area, the thing that you can do at this point in time that would most benefit you is to establish your base in the MFRS structure – especially the MFRS 3, MFRS 13, MFRS 136, and MFRS 2. Do not just read lists of standards but read them. Get to know why fair value is measured in the manner it is and the impact of hierarchy of inputs to the dependability of your findings. This should be supplemented with practical modelling practice, since no one can replace the judgement that may be gained by constructing and supporting a DCF model or a PPA model.

In case of mid-level professionals, the prospect is in further specialisation. Whether that is becoming an expert to whom the intangibles valuation, impairment test, or share-based payment models are a specialty, depth of understanding is well understood, and you will be far more attractive to the employers and clients alike. Take time to get to know how your Malaysia Financial Valuation Work is a part of the larger audit and financial reporting process – since people who can close the gap between valuation and accounting will never go out of demand. The profession is filled with professionals who are mentally inquisitive, respected in their paperwork, and able to articulate themselves effectively. Begin with that, and it will go on.