How Healthcare Startups Allocate Purchase Price

Introduction to How Healthcare Startups Allocate Purchase Price

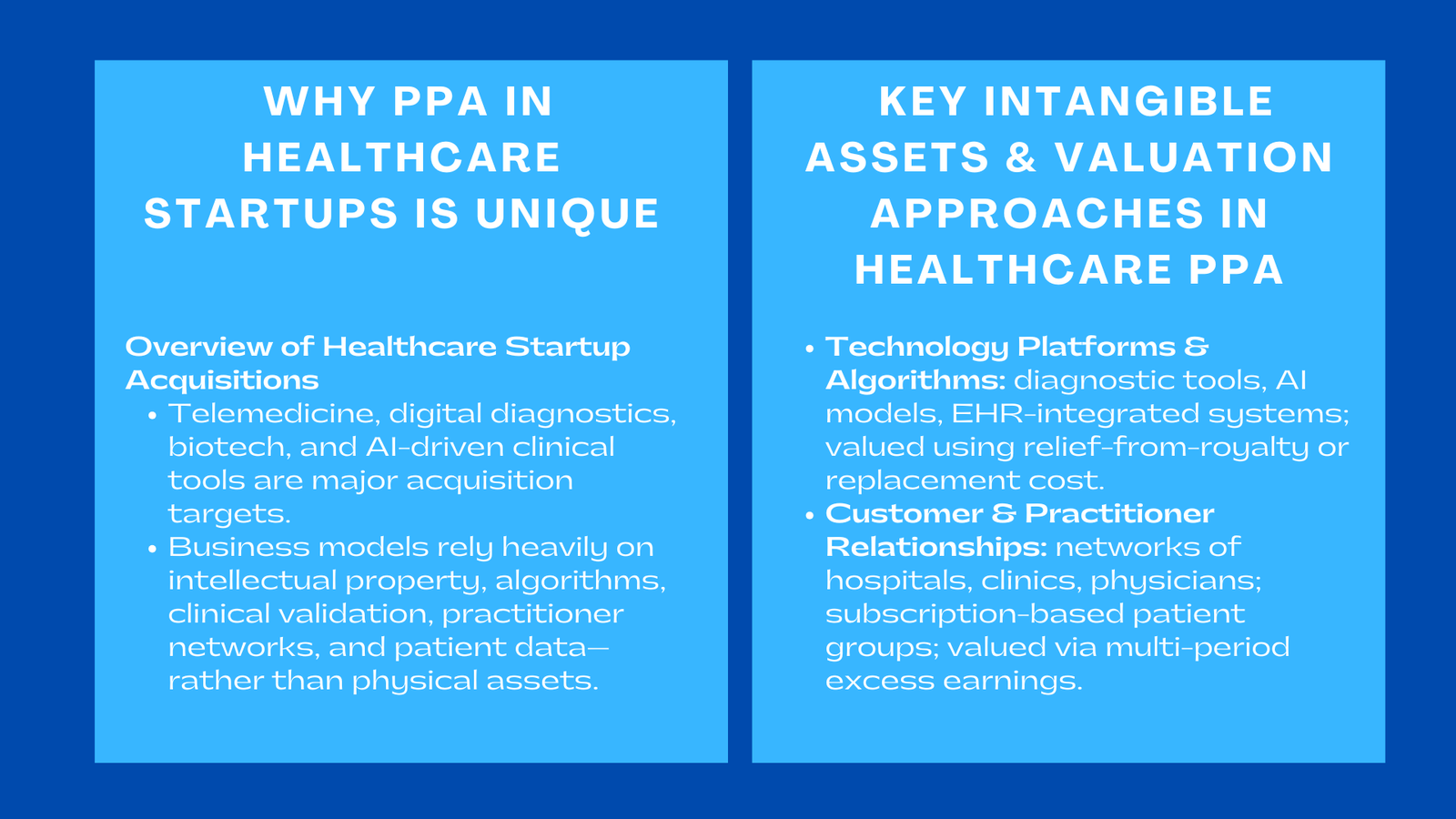

Startups in healthcare, such as telemedicine platforms and digital diagnostics companies, biotech innovators, AI-focused clinical tools are becoming an increasingly popular acquisition target as investors look to get exposure to rapidly growing healthcare technologies. These startups are characterized by complex business models, distinct business regulatory settings and meaningful intangible value in their intellectual property, customer relationship and clinical information resources, making them a strong focus area for any purchase price allocation valuation Singapore firm.

When healthcare startup is being acquired, one of the most important post-acquisition procedures is the assignment of the price of purchase. According to the IFRS 3, the acquirers are required to recognize and determine the fair value of all the assets, both tangible and intangible assets, as well as goodwill. This paper focuses on a single area in this process the allocation of purchase price to identifiable intangible assets in healthcare startups. Since the assets of the healthcare sector are not similar to the ones of the traditional industries, valuation analysts have to use specialized techniques, stringent compliance factors, and the sector-specific judgement to effect the right recognition.

1. Learning What Healthcare Startup Assets Are.

1.1 The reason why Purchase Price Allocation is more complex in Healthcare.

Healthcare startups do not usually work with big amounts of physical investment. They have value in most cases that consists of intellectual property, software platforms, algorithmic model, clinical validation procedure, practitioner networks, regulatory approvals and proprietary patient data. This is compounded by the fact that most of these assets have regulatory controls, continuous developmental cycles and commercialisation trajectories which are long term.

During healthcare startup purchase price allocation, analysts often encounter intangible assets such as clinical algorithms, regulatory submissions (e.g., FDA 510(k) equivalent data), treatment protocols, proprietary sensors, and digital health application frameworks. Such assets demand special valuation methods which include the scientific uncertainty and probable future scalability.

1.2 Calculability of Allocable Assets by Regulatory Environment.

The sphere of healthcare is highly controlled through regulations that come in various forms such as patient data privacy laws, medical device certification standards, and so on. This regulatory environment affects the recognition of the assets. As an example, the value of clinical datasets obtained in the process of interaction with patients can exist, but it must be in a compliant and transferable form.

Likewise, any new technology that facilitates telehealth consultation, remote monitoring, or AI-assisted diagnosis can have high levels of intangible value, but is risky in the case of regulatory approvals being pending or incomplete. The treatment of such assets affects their fair value and shape of amortisation under IFRS M&A reporting, especially when future cash flows depend on regulatory milestones.

2. Identifying Intangible Assets Unique to Healthcare Startups

2.1 Technology Platforms, Algorithms, and Software

Numerous health technologies establish their own software systems, which combine clinical guideline and diagnostic algorithms, electronic health record (EHR) data and patient management applications. Such platforms have to be valued by isolating the codebase underlying them, their algorithmic layers, and their embedded clinical logic.

Other startups can also own patented medical equipment or machine learning models that have been trained on massive datasets. These assets are fair-valued by the uniqueness, defensibility, and scalability of these assets. Valuation is commonly based on the relief-from-royalty technique or replacement-cost estimates which map engineering work, regulatory checking as well as commercialization prospects.

2.2 Customer and Practitioner Relationships.

Healthcare startups can also be based on the network of hospitals, clinics, physicians, or insurance companies. Such relationships are economic resources since it helps to generate repeat consultations, subscription income, or procedure volumes.

Contracts between customers and practitioners should be evaluated in terms of length, renewal possibilities and revenue streams. Customer relation assets identifiable in digital health and telemedicine startups are also subscription-based patient groups or user groups.

2.3 Clinical Data Assets

Proprietary clinical data is becoming a point of view in healthcare acquisitions. Such data sets can have anonymized patient history, diagnosis, care, or even biomarker trends that are captured by medical equipment or apps.

The problem in the valuation is whether such information can be transferred, is ethical and is legally acceptable to be monetized by the acquiring entity. In that case, it is separate intangible asset because it can be used to facilitate algorithm training, product development, or licensing partners.

3. Best valuation practices in response to healthcare startups.

3.1 This section evaluates a clinical technology based on its income.

In the case of mature clinical technologies or diagnostic platform, the income-based approaches are generally employed. Forecasted cash flows encompass software licencing fee, clinical service income or diagnostic access charge. Risk adjustments are indicative of regulatory risk, clinical effectiveness and competitive forces.

Multi-period excess earnings techniques are those that capture customer relationship resources where future patient volumes or retention of subscribers give stable earnings streams.

3.2 Relief-from-Royalty of Patent and Software.

Usually patented devices, proprietary algorithms and advanced EHR solutions apply the relief-from-royalty method. Licensing arrangements of similar software or devices have to be benchmarked by analysts. The royalty rates are based on uniqueness of technology, levels of clinical validation and replaceability in the healthcare ecosystem.

3.3 Early-stage Research Asset Cost Approach.

At the nascent or pre-commercial stage of technologies, cost-based methods might be necessary. These are apprehended growth endeavor, clinical trial spending, device prototyping, and regulatory submission expenses that is necessary to reproduce the asset.

Since healthcare startups in the initial stages do not always have predictable sources of revenue, this method offers a justifiable source, as well as considering the risk of development.

4. Fair Valuing of Healthcare Startup Intangibles.

4.1 Separating Core Technology and Goodwill

Of particular importance is the difference between identifiable assets and goodwill. Goodwill can be separated off technology or data that create economic benefits, however, such factors as workforce expertise, promise made by a brand without a registered trademark or reputation of a clinical team usually fall within the category of goodwill.

The allocation rationale has to be justified by the analysts so that it is in accordance with IFRS 3 and is also able to be audited particularly by the private equity buyers who might require quick post-acquisition scale.

4.2 Determination of Useful Life of Clinical and Digital Assets.

Healthcare startups rely more on useful life estimation. In a few years, clinical technology might be becoming obsolete as a result of new research, competitors or changes in regulation. On the other hand, clinical workflow algorithms that are validated can have a longer economic payoff.

The relationships of customers to healthcare providers tend to have long useful life as they find switching to be expensive particularly when it comes to integrated diagnostic or telemedicine system.

4.3 Consideration after acquisition.

Once allocated, healthcare startups will have to match financial reporting with operating realities. With changes in clinical performance, there are new requirements or the model of reimbursement changes, the acquirer should test impairment regularly, and also re-evaluate the values of assets.

Acquisitions within the healthcare are very sensitive in terms of clinical outcomes. The adoption of a diagnostic tool is poor or there are delays by the regulators, which can result in impairment, showing the significance of sound forecasting.

Conclusion

When making an allocation of purchase price in healthcare start ups, one should understand the clinical technology, regulatory environment, customer networks, and value models that are data-driven. Intangible assets take center stage in valuation and separability of technology, customer relationship and clinical data is the key to transparent and defensible allocation results. Acquisers can provide accurate reflection of the economic reality of the healthcare startup in the post-acquisition financial reporting by assessing it in a disciplined manner and through adherence to the requirements of IFRS.