PPA Valuation Impact on Financial Reporting

Picture 1 : Understanding Purchase Price Allocation

In the case of an acquisition between two companies, the deal does not close with the deal signing. As a matter of fact, the process of deciding how to apportion the purchase price to the assets and liabilities of the acquired company commences immediately after. Such allocation is called purchase price allocation and it is not just a formality of accounting. It determines the appearance of the financial statements of a company over several years, impacts on the rating of the performance by analysts, and has a direct impact on the decision made by investors, lenders, and regulators.

PPA valuation lies on the crossroad of financial reporting, business valuation and corporate strategy. Under the accounting regulations like the IFRS 3 (Business Combinations) and ASC 805 (the US GAAP counterpart), acquirers must recognise the identifiable assets acquired and liabilities obtained at their fair values at the acquisition date. This necessity leads to the development of a good body of work, finding intangible assets that might not have been reflected on the balance sheet of the target, and valuing them as well as providing the results that can be justified to the auditors and regulators.

To junior to mid-level professionals joining finance, accounting, or advisory services, knowledge of PPA valuation and its implications on the financial reporting transparency is becoming more and more relevant. The M&A activity does not demonstrate any deceleration and the popularity of professionals able to cope with technical and commercial aspects of the allocation of the purchase price is increasing. This paper defines the main concepts, steps in the process, provides practical examples and lessons learned, and also some practical advice to practitioners who develop their expertise in this field.

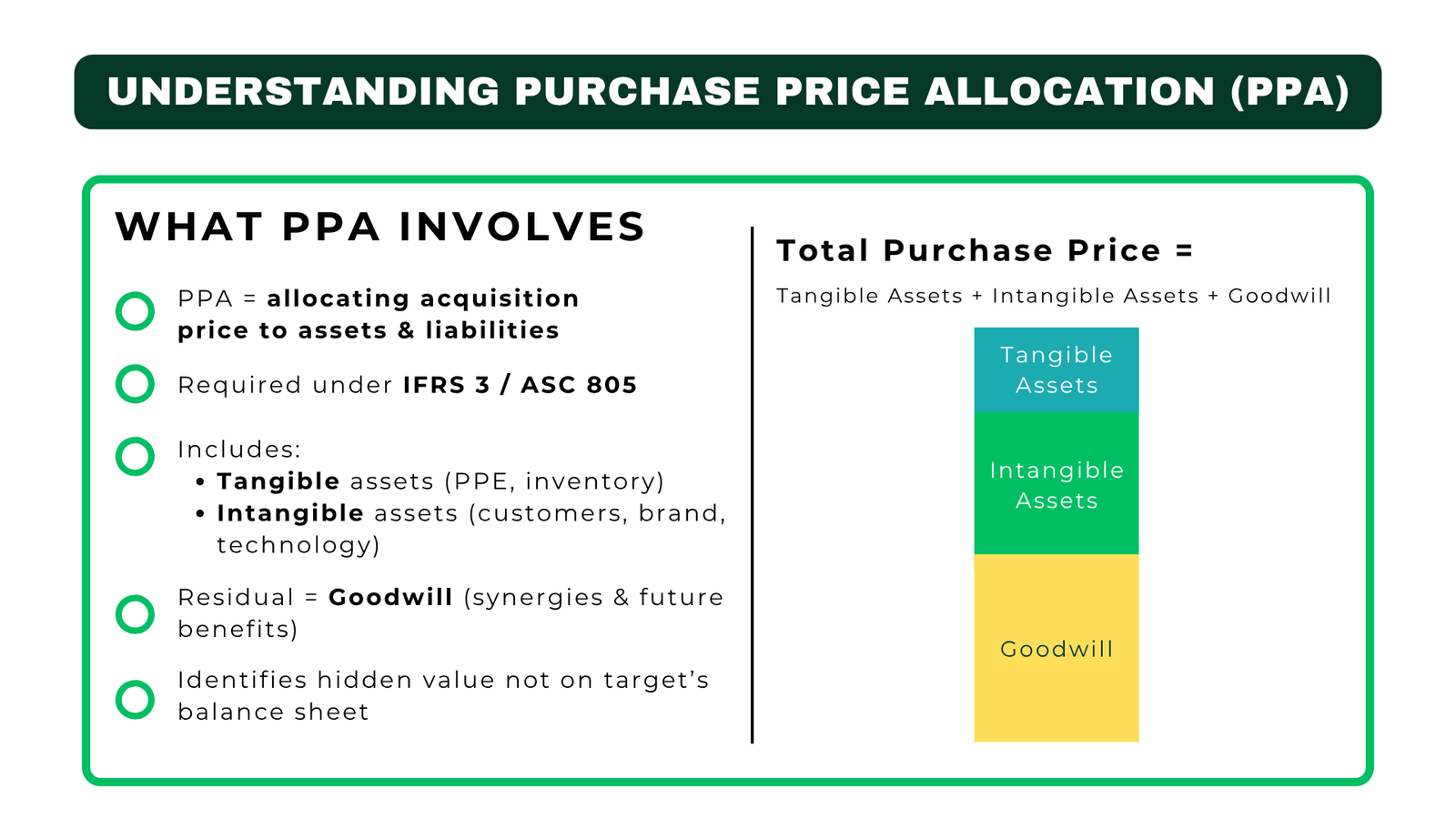

What Purchase Price Allocation Involves

Purchase price allocation is a fair value exercise at its very core. In the event that a business is sold to a company, the total consideration made up of cash, shares, deferred payments, and contingent consideration should be apportioned to the assets purchased and liabilities incurred. The first step involves the identification of all the physical assets: the property, plant, equipment, inventory and receivables. However, the more complicated and consequential endeavour would be the recognition and recognition of intangible assets that the target company may never have recognised on its balance sheet.

The intangibles may be relationships with customers, developed technology, trade names, favourable leases, non-competence agreements, and order backlogs. All these should be recognised separately in case they can be distinguished that is, they are not part and parcel of the business or they are generated by a contractual or legal claim. The valuation practitioners at PPA have different methodologies that they use to value each category: the multi-period excess earnings method (MEEM) in customer relationship, the relief of royalty in trade name and cost or replacement in assembled workforce and in some other asset.

The remaining value of the allocation value to all the identified net assets is subject to goodwill. Goodwill is the amount an acquirer is willing to pay to take the identified synergies, strategic positioning, and economic benefits yet to be realized that cannot be identified and measured separately. In both the IFRS and the US GAAP, no amortisation of goodwill is done, but rather, goodwill undergoes an annual impairment test. The allocation of purchase price to create the split between finite lived intangibles (which are amortised and decrease reported earnings) and goodwill is basic to the financial reporting impact of any acquisition.

Table 1: Common Intangible Assets Identified in PPA and Typical Valuation Methods

| Intangible Asset Type | Valuation Method | Useful Life (Typical) |

| Customer Relationships | Multi-Period Excess Earnings Method. (MEEM). | 5–15 years |

| Trademarks/Trade Names. | Indemnification Royalty Method. | Indefinite or 10–20 years |

| Developed Technology | Relief-of-Royalty/ Cost Method. | 3–10 years |

| Non-Compete Agreements | Lost Profits / Income Approach. | Duration of agreement |

| Order Backlog | Multi-Period Excess Earnings Method | Under 1 year |

| Favourable Leases | Discounted Cash Flow (DCF). | Time to expiry of lease. |

| Goodwill (residual) | Not individually valued – residual. | Permanent (impairment test) |

Five Key Steps in a PPA Valuation Engagement

A disciplined sequence of purchase price allocation is well executed. The following steps are typical of most advisory firms, audit groups and corporate finance departments worldwide.

Step 1: Define the Acquisition Date and Consideration

The date of the acquisition is the day when the acquirer gains the control over the business that is acquired. All fair values measurements are to be done as at this date not at signing, not at close documents, but at the moment control is transferred. The consideration involves not only cash but also shares issued on fair value, contingent consideration (i.e. earn-outs) and any equity interest that may have been held before. The consideration calculation is a base case, as all other steps in the PPA valuation descend out of it.

Step 2: Record All the Acquired Assets and Liabilities.

The second move would be to create an in-depth inventory of all that the bought entity possesses. This is far beyond the balance sheet of the target. These intangible assets that had been internally developed and thus never recognised under previous accounting standards are surfaced by management interviews, customer contract reviews, technology audits and legal diligence. It must be done in a systematic way, failure to recognize an intangible asset in a purchase price allocation may result in financial statements restatement, or regulatory issue.

Step 3: Use Relevant Methodologies of Valuation.

Once the entire list of identifiable assets is developed, the valuation professional implements the most suitable methodology to every one of the assets. The MEEM is generally used to value the relationships that one has with the customers after deducting all the other assets that contribute to such relationships. The relief form is commonly the most commonly utilized method of valuing trade names and is a method of estimating the royalty that a company would pay to license the name had it not owned it. The method is to be justified, documented and consistent with the assumptions of the market participants- an essential prerequisite of valuation in the financial reporting transparency.

Step 4: Decision of Discount Rates and Significant Assumptions.

Every intangible asset has its risk profile and the discount rate applied in order to present-value the future economic benefits of the asset should capture that risk. There are chances of discounting customer relationships that have high levels of renewal and a long history at rates that are near the weighted average cost of capital (WACC). Liquid assets like technology in a rapid moving industry might have to be charged much higher. These assumptions should be recorded, they should be compared to the evidence in the market and checked by auditors. Here PPA valuation becomes truly complicated: even minor modifications in the assumption about discount rates may change asset values – and consequently amortisation charges in the future – by tens or hundreds of millions of dollars.

Step 5: Prepare, Examine and Record the Allocation.

The last thing to do is to prepare the complete allocation schedule and ensure that the net assets identified and goodwill that are found against the consideration paid are the same and then finally create a report that records all the decisions that were made in regards to assumptions, data source, and methodology. This documentation can be used in a variety of ways: it allows the audit, meets the expectations of the regulations, and forms the basis of any future impairment analysis. One of the professionals who will excel in this profession is those that have realized that the valuation that is needed to be reported in terms of transparency must be done with strict documentation and not with technically correct figures.

Process Flow 1: End-to-End PPA Valuation Workflow

| Phase | Key Activities | Responsible Parties | Typical Timeline |

| Pre-Deal Scoping | Scopes definition, target financial gathering, terms of engagement agreement. | Advisor / CFO | Pre-signing |

| Data Collection | Management interviews, contract audit, IP audit, legal diligence. | Advisor + Target Mgmt. | Weeks 1–3 post-close |

| Asset Identification | Identify all physical and intellectual assets; identify recognisability. | Valuation Team | Weeks 2–4 |

| Valuation Modelling | Use MEEM, RfR, cost techniques; find discount rates. | Valuation Analyst | Weeks 3–6 |

| Review & Challenge | Auditor exam, assumption benchmarking, sensitivity testing. | Auditors + Advisor | Weeks 6–10 |

| Finalisation & Report | Prepare allocation schedule; prepare report of valuation to be filed. | Advisor + Audit Team. | Weeks 10–12 |

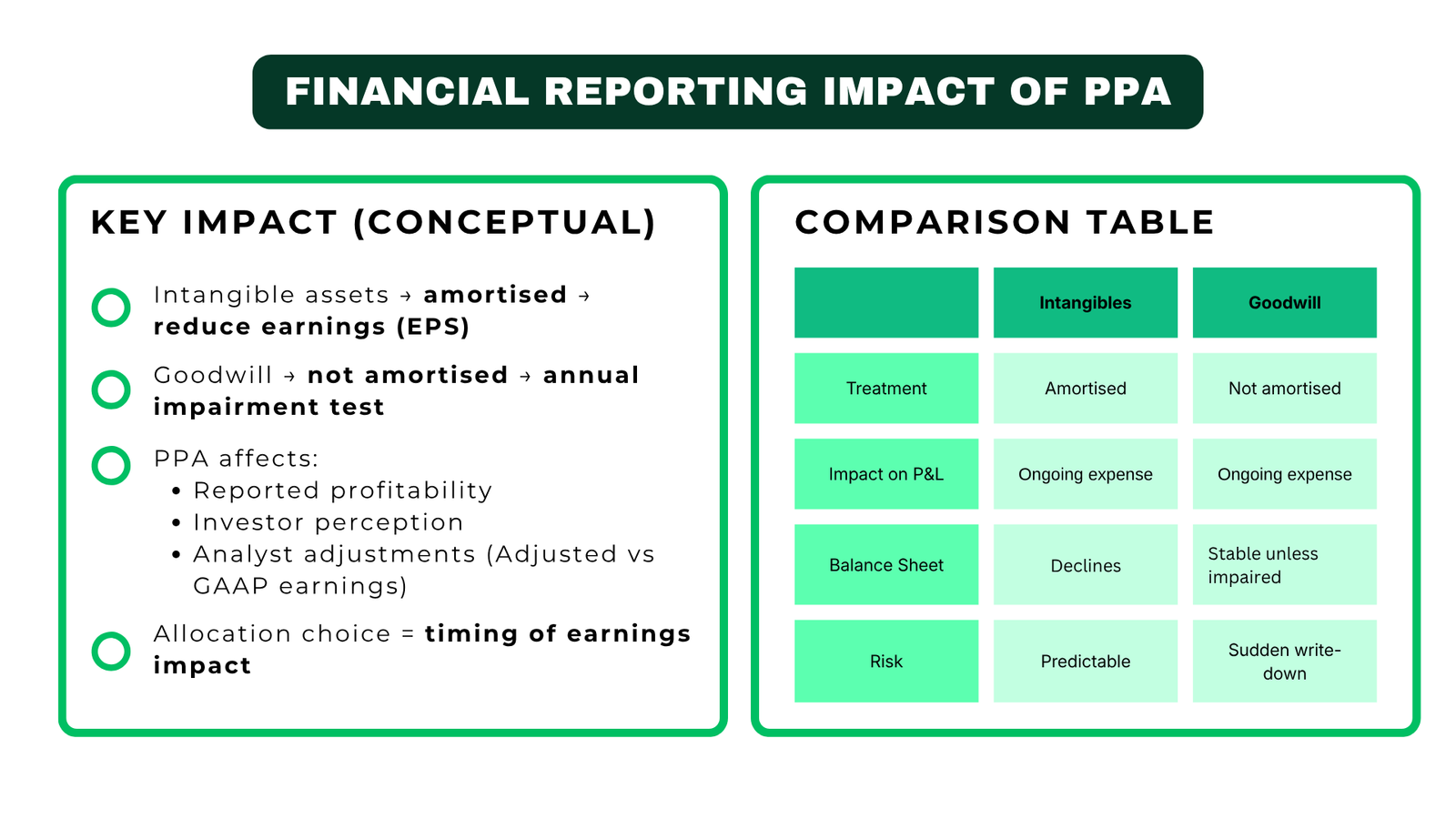

How PPA Valuation Shapes Financial Reporting Outcomes

Picture 2 : Financial Reporting Impact of PPA

The purchase price allocation has both financial reporting implications which are both long-term and impactful. After recognition and allocation of useful lives of intangible assets, the amortisation is carried out using the income statement which declares reported earnings in each period until the asset is fully written off. This is to say that a firm that engages in a significant acquisition might record reduced earnings per share in the number of years not because the business is performing poorly, but due to the amortisation of intangibles realised in the purchase price allocation process.

This dynamic has significant implications on how the financial analysts analyze the reported results. A large proportion of advanced investors and analysts recalculate reported earnings by reinstating amortisation of acquisition-related intangibles to get what they believe to be a more significant indicator of operating performance. This difference, between GAAP earnings and adjusted earnings, is important in understanding why the decisions in PPA valuation are significant to professionals, not just to those in the commercial aspect, but in the technical aspect as well. A firm which assigns larger value to intangibles which have shorter lives will record lower earnings sooner; a firm which assigns larger value to goodwill will not amortise and will have risk of impairment.

Goodwill is treated in a rather consequential manner. According to the IFRS, goodwill is impaired after every year at the cash generating unit level. In the US GAAP, the same annual impairment test occurs on a reporting unit level. In the event of decline in business performance or change in market conditions, goodwill impairment charge may be large- billions of dollars in the case of large acquirers. The charges pass directly through the income statement and can have a very large impact on the stated profitability. The impairment charge of about US 15 billion that Kraft Heinz took in 2019 is a clear reminder that decisions that are made during the period of the acquisition in terms of valuation and the goodwill that are generated by them can be felt in the financial statements long after the transaction has taken place.

Table 2: Financial Reporting Impact — Finite-Lived Intangibles vs. Goodwill

| Characteristic | Finite-Lived Intangibles | Goodwill |

| Accounting Treatment | Amortised useful life. | Not amortised; Annual impairment test. |

| P&L Impact | Routine amortisation expense diminishes profits. | Any impairment charge decreases earnings. |

| Balance Sheet | Amortisation decreases gradually. | Unimpaired except when impaired. |

| Management Preference | In most cases, less is preferred (to guard profits) | Generally wants more (shares P&L impact) |

| Auditor Focus | Useful life and methodology assumption. | Assumptions of impairment testing. |

| Analyst Adjustment | Frequently subtracted in the calculation of adjusted EPS. | The impairment reversed in adjusted figures. |

Real-World Examples and Lessons Learned

Real dealings shed light on the way in which decision on allocation of purchase price works out in reality and the outcomes that arise when such decisions are subsequently appealed or overturned.

A case in point is the acquisition of Time Warner by AT&T in 2018 at about US 85 billion. The acquisition price gave high values to programme content assets, customer relationship and the brand names of AT&T and HBO. These intangibles gave rise to high annual amortisation charges that burdened on the reported earnings. A few years later, when the company underwent strategic modifications and finally a spin off of the WarnerMedia, the company had to re-examine a lot of its initial allocation assumptions. The lesson to the professionals is that PPA valuation is not a one-time operation- it causes financial statement implications that need to be handled and clarified to the stakeholders over a long period of time.

The case of Microsoft and LinkedIn acquisition in 2016 worth around US 26 billion is a contrasting view. The analysts then expressed doubts as to whether this was a justified price considering that LinkedIn was not maximising its commercial potential yet. The allocation of value of the purchase price by Microsoft revealed that LinkedIn had substantial values in the number of its members (as a type of customer relationship), its technology base and its trade name. The next financial report recorded big charges on amortisation but also overtime, it revealed the revenue synergies that the management of Microsoft had forecasted. In this case, the valuation for financial reporting transparency served a twofold purpose of not only meeting the regulatory and audit obligations but also presented a written justification of the acquisition premium that the management would refer to when the business was in operation.

The healthcare sector is a good example of a warning story. In other cases, pharmaceutical companies have been subject to audit of intangible assets that, in purchase price allocation, were in-process research and development (IPR&D), and subsequently the asset was written down or impaired since clinical trials did not succeed or the product was not approved by the regulatory authorities. It happened in instances like these that the initial PPA valuation assumptions were too optimistic and the investors and regulators doubted whether the valuations had been done with enough rigour and independence. This highlights one of the core pillars: PPA valuation should be based on assumptions and realistic probability-weighted circumstances of the market participants, rather than on best-case assumptions as projected by management.

Process Flow 2: Intangible Asset Identification and Recognition Decision

| Decision Point | Question to Answer | Outcome if Yes | Outcome if No |

| Contractual / Legal | Is the asset of a legal or contractual nature? | Be intangible, identify separately. | Go to separability test. |

| Separability | Is the asset sellable, transferable or licensable? | Be intangible, identify separately. | Be not recognised separately. |

| Reliable Measurement | Is it possible to measure fair value? | Valuation and recognisation. | May transfuse into goodwill. |

| Useful Life | Is the life of the asset finite or not? | Amortise of useful life ( finite ) or impairment-test ( indefinite ). | N/A |

| Materiality | Is it a material value to the total allocation? | Complete valuation and disclosure necessary. | May add together with other akin assets. |

Challenges, Common Pitfalls, and How to Navigate Them

In spite of the well-defined accounting standards and proper valuation methodology, PPA valuation is among the more difficult aspects of financial reporting. There are a number of recurring problems which bring professionals and organisations to their knees.

The tension between rigour and speed is the most widespread. The transactions are closed under strict time lines and the management is often in a hurry to proceed with integration and often lacks the understanding of time and expertise involved in conducting a careful purchase price allocation. The measurement period of the PPA is up to twelve months under the IFRS 3 and ASC 805. This is a handy window, though it is not used to the full extent. Those professionals who are aware of this timeline and insist on proper resources at the very beginning will produce more justifiable results and will not have to go through expensive revisions.

The second common obstacle is subjectivity of intangible assets valuation. Judgement is involved in customer attrition rates, benchmarks in royalty rates, assumptions of technology obsolescence and discount rates. When these assumptions are questioned by auditors, which they always do, one has to base the answer on market data that can be observed not internal expectations. It is not an option to build a strong data file, which records the origin of each major assumption; rather, it is the core of valuation for financial reporting transparency and defence against audit challenge or regulatory review.

The third difficulty is the interaction of purchase price allocation and tax. Most jurisdictions have disparities between the valuation of assets to be used in accounting and the valuation used to determine tax. The amounts of deferred tax liabilities based on the step-up in value of intangible assets may be large and need to be included in the allocation model. The neglect of the tax aspect is a weakness that most novice practitioners commit and it may cause the purchase price to be allocated at the wrong time. Those professionals who form facility on both the accounting and tax aspects of PPA valuation will be much more effective in practice.

Conclusion: Actionable Insights for Professionals

Among the most significant valuation activities in corporate finance is purchase price allocation. The outcomes of a PPA valuation flow has direct effects on financial statements, influence reported earnings over years, influence how analysts and investors evaluate performance, and represent the basis out of which future impairment tests will be done. It is not about doing it wrong or right, both commercially, technically and reputationally.

To junior or mid-level professionals in their careers, a number of steps can be taken that will help them develop in this area quicker. One, take time to learn IFRS 3 and ASC 805 inside and out- not only the principles outlined in the headline, but what is required of the measurement and in what level of detail, as well as what the measurements period permits. These standards are the framework on which all PPA valuation work is carried out, and the knowledge of them means professional competency. Second, acquire realistic modelling skills within the respective methodologies, which would be applied in valuing intangible assets; MEEM, relief of royalty and income-based methodologies. Differentiating skill is the spreadsheet skill in creating such models, rather than filling in templates.

Third, learn to read purchase price allocation disclosure in filing of public companies. Listed companies which have made acquisitions must also report their PPA findings, the values which have been attributed to each type of intangible assets, the useful life which they have assigned and the amount of goodwill recognised. The intuition created in the analysis of such disclosures is how various industries and types of deals lead to different allocation results. Fourth, work with the audit and regulation aspects of this work. What acceptable valuation in the context of financial reporting transparency would appear to have in practice in the United States as per the expectations of Big Four auditors and the Securities and Exchange Commission (SEC) or other relevant regulators in other countries. Knowing these expectations at the beginning of your career will form the way that you treat each engagement.

Fifth, develop skills to present complicated valuation findings to non-experts in a way that would be understood. Board members, CFOs and audit committees must know the financial reporting consequences of a purchase price allocation without having to go through a lot of technical language. The person who is able to render findings of PPA valuation into normal words, as well as why a certain intangible should have been valued at a given amount, what will the amortisation impact will be, and what will be the impact on adjusted and reported earnings will be useful to any organisation that is going through a significant acquisition.

Finally, PPA valuation is a field of work that is interested in a curious mind, discipline, and a passion to understand numbers and business. With M&A becoming increasingly part of the international scene and with the continued use of accounting standards that increasingly focus on the need to assure valuation for financial reporting transparency, individuals who master the discipline will be at the heart of some of the most financially important tasks in the business.