Purchase Price Allocation in Business

Purchase Price Allocation in Business Introduction

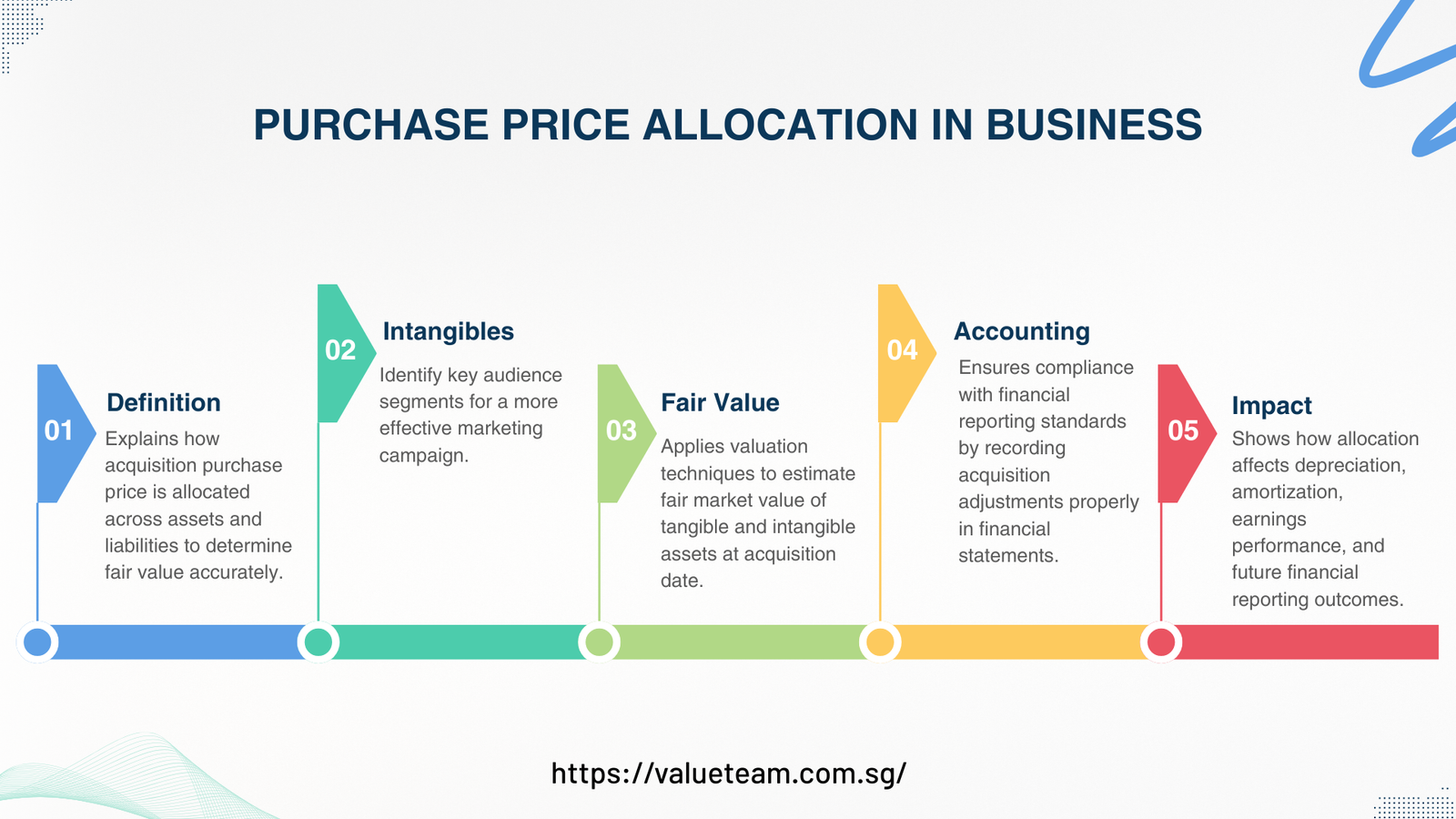

Being a new merger and acquisition, financial transparency and accuracy of valuation are no longer a matter of choice; they are essential pillars of governance and investor trust. Purchase price allocation purpose is one of the most important processes that occur after the transaction and this is used to ascertain how the total consideration paid during an acquisition will be attributed to identifiable assets, liabilities, and goodwill. With the growth of the regulatory control and the development of the accounting standards, the participants of the acquisition process need to be aware properly of not only the essence of the purchase price allocation process but also the reasons why it is needed and the effects it has on the long-term financial performance.

Global accounting standards including IFRS 3 and ASC 805 have made purchase price allocation sale of business a normal practice in acquisitions and divestitures as well as corporate restructuring. Meanwhile, customer relationship valuation of intangible assets, especially purchase price allocation, is a determinant of after-acquisition earnings, amortization profiles and exposure to impairments.

The paper considers the strategic, accounting and valuation basis of purchase price allocation, its application in the sale of business and how customer relationships are treated as identifiable intangible assets. The knowledge of these principles will help organizations to reach regulatory compliance and contribute to informed decision-making and sustainable value creation.

Strategic Meaning of Purchase Price Allocation

Purchase price allocation is not just accounting in nature. In essence, purchase price allocation purposeis to transform a negotiated transaction price into a practiced financial disposition of a obtained business. The process will make the stakeholders to be aware of what has been purchased, how the value will be shared among the assets, and how the economic benefits are likely to be achieved in the long run.

In takeover deals, the purchasers often buy at a premium. This premium is based on the expected synergies, brand-strength, customer loyalty, proprietary technology and positioning of the product. Purchase price allocation clearly identifies such value drivers by distinguishing between the tangible assets, identifiable intangible assets, and goodwill. The economic reasonability of a transaction will not be apparent to investors, auditors and regulators unless they have a disciplined allocation process.

In a strategic manner, purchase price allocation assists in decision making in capital allocation, post merger integration planning and also measurement of performance. By disaggregating the source of value in its assets, the management can be able to devote investments and reduction of risks in a more efficient manner.

Accounting and Regulatory Foundations

Global accounting regulations require purchase price allocation whenever doing business combinations. According to these standards, the acquired assets and assumed liabilities shall be valued at fair value using the date of acquisition. This demands the purpose of transparency, comparability and consistency of financial reporting in purchase price allocation.

Compliance in purchase price allocation sale of business is not a choice. Poor or improper allocation may lead to audit observations, financial restatements or sanctions. More importantly, poor allocations may be used to misrepresent earnings by making incorrect amortization or impairment claims.

The regulators and auditors are increasingly demanding that valuation methodologies should be strong, documented, and supported with market data in addition to being consistent with accepted valuation standards. This has seen purchase price allocation become a multidisciplinary undertaking that integrates accounting, valuation, strategic analysis and industry experience.

Purchase Price Allocation in the Sale of a Business

Purchase price allocation sale of businessis used in case a majority interest in a company is sold to a new owner. In the case of transactions of this nature, the buyer should divide the purchase consideration based on the fair values of the assets acquired and the liabilities incurred between the two at the date of acquisition.

This is the process of determining all tangible and intangible assets, which have been acquired and these include property, inventory, contracts, intellectual property and assets relating to customers. Both financial and operational liabilities should also be at fair value. Any value remaining after allocation is taken to goodwill.

This allocation has a direct impact on post-acquisition financial reports. The allocation of depreciation and amortization expenses affect the historical profitability that is reported, whereas goodwill and indefinite-lived intangible assets are also currently tested through impairment.

Even though purchase price allocation is largely a demand of the buyer, sellers also have the advantage of knowing what will be allocated, since this may influence the negotiation of the transactions, tax issues, and even the representations of the sellers when selling their goods.

Recognition and Identification of Intangible Assets

One of the most complicated issues of purchase price allocation is the identification and valuation of intangible assets. Intangibles do not have a physical appearance in contrast to tangible assets but in many cases do have a large transaction value.

The purchase price allocation customer relationship assets are often some of the most valuable of them. The customer relationship indicates the economic returns of the current customers to the organization, such as recurring revenues, contract renewal and cross selling.

Customer relationships have to be identifiable and must satisfy the criteria of separability or have to be initiated by contractual or legal rights in order to qualify as identifiable intangible assets. The relationships with the customers are evident to meet such requirements in many service-oriented and subscription-based businesses.

Customer Relationships valuation in PPA

The purchase price allocation customer relationship asset should be valued in close relation to analyzing customer behavior, customer revenue trends and customer attrition. The valuers are required to make an estimation of future cash flows which can only be attributed to the existing customers, but not to the acquisition of new customers or any other intangible assets.

Valuation methods that are based on income are commonly applied, separating the unwanted excess earnings through customer relationships. Such methods include customer revenue forecasting, removal of contributory asset charges and discounting to present value of the residual cash flows using risk-adjusted discount rates.

The assumptions of valuation should be reasonable, justified and aligned with the market data. Both excessively optimistic and excessively pessimistic assumptions can contaminate asset values and impairment risk in the future and increase future financial performance, respectively.

Association between Customer Relationships and Goodwill

There is a need to establish a sharp difference between purchase price allocation customer relationship assets and goodwill. Customer relationship can be distinguished as identifiable, finite-lived, intangible assets, which are liable to amortization, whereas goodwill is residual value, which is caused by synergies, expertise of the working force, and expectations of future growth.

Conflating customer relationships as goodwill may be rather costly. Goodwill is neither amortized nor tested but annual impairment testing, whereas customer relationship assets are tested to impact earnings through an annual systematic amortization. Rigorous classification makes financial statements representative of the economic reality and account to the standards of accounting.

This difference supports the bigger purchase price allocation aim of accountability and transparency in financial reporting.

Operational and Financial Consequences

Purchase price allocation has far reaching implications even after the transaction has closed. The amortization of intangible assets has an impact on the earnings trend, tax position, performance measures, whereas impairment test is used to determine the risk and investor confidence.

The results of allocation in purchase price allocation sale of business, can also have implications on the earn-out arrangements, management incentives, and covenant compliance. It is based on this reason that purchase price allocation must be incorporated in transaction planning as opposed to a post-deal issue.

Strategic purchase price allocation allows organisations to handle earnings volatility, communicate with stakeholders and value creation over the long term.

Documentation, Governance and Audit Readiness

Effective purchase price allocation is based on strong governance. The valuation documentation has to be straight forward about methodologies, assumptions, source of data and concluding commentary that can survive scrutiny by an audit committee and regulations.

The purpose of the purchase price allocation involves the generation of defensible and transparent valuations that are applicable across transactions. Governance frameworks must provide a regular re-evaluation of the assumptions and alignment with the changing accounting standards.

Integration of purchase price allocation governance into financial activities minimizes the chances of disagreements, restatements and loss of reputation.

Prudent Purchase Price Allocation Insights

In addition to compliance, purchase price allocation can be used to give insights in value creation. Knowledge of asset-level value drivers helps the management to optimize the integration strategy, increase customer retention efforts and investment in core competencies.

Purchase price allocation customer relationship valuations can be used to inform customer segmentation, pricing strategy, and lifecycle management. On the same note, the analysis in purchase price allocation sale of business transactions can inform acquisition plans and portfolio optimization in future.

Purchase price allocation is not a liability but turns out as a tactic when implemented wisely.

Trends on Purchase Price Allocation in Future

With the increasing data-drivenness and intangibility of business models, the role that purchase price allocation plays will only continue to become more important. The intangible assets are becoming more accurately valued thanks to the development of analytics, the availability of customer data, and valuation methods.

Meanwhile, transparency and governance expectations to the stakeholders are on the increase. The purpose of purchase price allocation will continue to go beyond the financial reporting to a wider communication to investors and other regulators about value creation and management of risks.

The modern day organizations that invest in valuation powers and robust processes will be in a better position to handle future complexity.

Conclusion

The purchase price allocation is part of the basis of transaction accounting and strategic financial management. Organizations become more transparent, compliant, and informed by establishing the purpose of allocating the purchase price. Purchasing price allocation sale of business also requires proper allocation of purchase prices to maintain the credibility of financial reporting and the sustainability of the performance of the company after the acquisition.

The purchase price allocation cost of valuation of customer relationship assets shows the increasing role of intangible value in the current economy. Purchase price allocation when done stringently and incorporated into governance structures enhances investor confidence, aids in strategic implementation and creation of long term value.