Top PPA Valuation Mistakes to Avoid

One of the most technically challenging activities in financial reporting is purchase price allocation. Accounting standards, mainly those of IFRS 3 and ASC 805, when one business acquires another stipulate that the purchase price be apportioned to all recognisable assets and liabilities at their fair values and the remaining portion should be recognised as goodwill. This is a structured and logical process in theory. Practically, it is a judgment-filled and data constrained, and modelled exercise. PPA valuation common mistakes are rife and most of them are not caught until they are uncovered under an audit scrutiny or worst still when it is too late in years under a goodwill impairment test.

In the case of junior and middle-level professionals operating in the transaction advisory/ corporate development/ audit/ financial reporting, it is equally important to know where PPA exercises fail as it is important to know how to do them well. The most common mistakes that occur in the field are hardly due to ignorance of the standards most are due to time constraints, incomplete information, misused methodologies and lack of coordination among legal, finance and valuation teams. Early identification of these patterns in your career makes you in a position to put in real value, raise red flags at the right time and not become the individual to sign off on a model which ends up crashing.

This paper takes a tour of the most prevalent and most impactful PPA valuation common mistakes, discusses the operations in which they most frequently occur, gives an example of how things have gone awry in practice, and offers advice on the way forward on working on the analysis of PPA modeling errors. You may be writing your first PPA or you may be re-reading your fifth but the lessons here will hone your professional judgment and assist you in coming up with a piece of work that can stand the test of time.

Understanding the PPA Framework and Where It Begins to Break Down

The purchase price allocation exercise are done in a prescribed format: compute fair value of consideration transferred at the acquisition date based on consideration, identify assets and liabilities acquired and assumed, value each at fair value and compute goodwill as the difference between total consideration and net fair value of identifiable net assets. Even though this framework is properly developed, the execution is the devil. The most significant PPA valuation fallacies are often the ones that are made at the beginning of the scoping process, not on the ultimate figures, but what to consider as an asset, what methods to use, and what data to trust.

Intangible asset identification is one of the initial and most important ones. According to IFRS 3, the acquirer is to recognise intangible assets separately of goodwill where they satisfy either the contractual-legal requirement or the separability requirement. Practically, most preparers do not classify all the range of intangible assets that are eligible to be classified. All candidates are customer relationships, technology platforms, trade names, non-compete agreements, favourable lease agreements and order backlogs and missing any one of them can meaningfully alter the allocation. The following table describes some typical types of assets, the most common valuation techniques and the most common errors that can be made with each.

| Asset Category | Examples | Valuation Method | Common Mistake |

| Customer Relationships | Agreements, subscriber databases, distribution networks. | Multi-Period Excess Earnings (MPEEM). | Inflating retention rate and revenue term. |

| Technology / IP | Computer software, patents, proprietary process. | Relief-from-Royalty approach or Cost approach. | Applying non-sector benchmarked royalty rates. |

| Trade Names / Brands | Brand identities, product trademarks. | Relief-from-Royalty | Inflation of brand value with goodwill. |

| Order / Backlog | Signed orders, committed pipe. | Income methodology – direct revenue attribution. | Risk of disregarding contract cancellation. |

| Non-Compete Agreements | Restrictive covenant of key personnel. | With-and-without method | Arguing that the enforcement is 100 per cent. with no discount. |

What is significant about the pattern that arises out of this table is that PPA modeling error analysis indicates that there is always a pattern in which mistakes are not idly present. They tend to congregate around particular assets – especially customer relationships and technology – in which there are the greatest subjective assumptions about future success. The less certain the future cash flows are, the greater the risk that an analyst will either be anchoring on overly optimistic projections or under time pressure will default to industry averages that are not appropriate to the particular business being acquired.

Five Critical Mistakes That Undermine PPA Quality

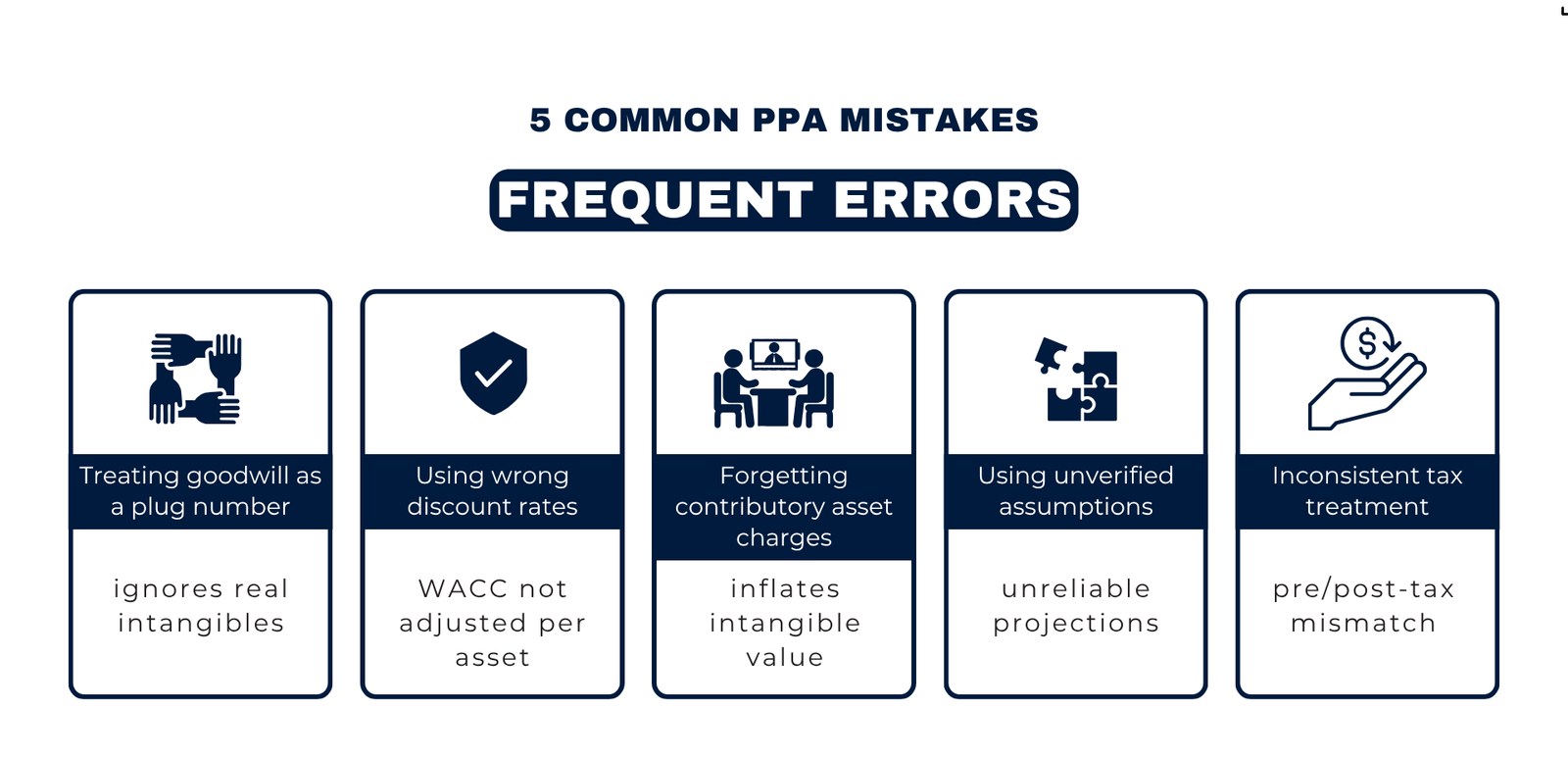

Picture 1 : 5 Common PPA Mistakes

The five mistakes that are described below are the most effective and common problems that have been found in PPA exercises in different parts of the world. The right process discipline can be applied to each of them, yet they all must be prevented through conscious effort. They are the main part of any serious PPA modeling error analysis.

Mistake 1 — Treating goodwill as a catch-all residual. The residual is by definition goodwill, but it must be the number left over at the end of the model, not a predetermined target calculated then to explain why the other model parts have reached the desired level. By not taking the time to identify all identifiable intangibles, but going directly to the goodwill calculation, preparers run the risk of understating identifiable intangibles and overstating goodwill. This results in a problem of deferral: inflated goodwill is vulnerable to impairment which can cause high charges to the income statement in subsequent years. This issue has become a major concern of auditors and regulators in a number of jurisdictions have provided guidance on this matter specifically about the risk of inadequate intangible identification.

Mistake 2 — Wrong or undue discount rates. All the intangible assets within a PPA model are discounted at a rate that is reflective of the risk profile of the intangible asset. The weighted average cost of capital (WACC) is not a destination, it is just a starting point. The assets with higher risk e.g. the in-process research and development or early customer relations should be discounted at more than WACC. An asset like net working capital has less risk and should be discounted at a lower level that is near to risk-free rate. In the situation where analysts use the WACC to price all assets in a similar way, they price the portfolio systematically wrong. The WACC-to-WARA reconciliation is a fundamental test in any PPA modeling error test, the weighted average return on assets (WARA) ought to be near the WACC. Otherwise, there is something wrong.

Mistake 3 — Missing or incorrectly calculating contributory asset charges. Multi-Period Excess Earnings Method (MPEEM) – This is the most popular method to value the relationship with customers; the technique involves the deduction of contributory asset charge (CAC) on the estimated cash flows and then this is discounted. The CAC is the economic payment that supporting assets (working capital, fixed assets, workforce) are entitled to making their contribution to the creation of those cash flows. Leaving out a CAC or failing to compute it properly exaggerates the value of the intangible being modelled. This is among the most technically delicate sections of PPA valuation error zones, and one in which even accomplished professionals can shirk corners when they are under deadline pressure.

Mistake 4 — Making assumptions of unreliable or untested input. The better the inputs, the better is a PPA model. All the assumptions must be based on verifiable data, i.e., on management accounts, churn analysis, industry databases, and the like transactions, which include customer attrition rates, royalty rates, increase in revenues, as well as the remaining useful lives of the equipment. The model does not reflect reality in the economy when based on the dreams of the management or the pattern of history, or on company-peculiar data or on generic level data. This happens especially in fast-paced industries like the technology and healthcare fields where growth stories may engulf analytical rigour.

Mistake 5 — Inequality of tax treatment within the model. PPA exercises make both taxable and tax-free calculations, the liability of deferred tax, and the use of that the intangible amortisation is tax-deductible in the applicable jurisdiction. Mismatches in tax treatment, such as the application of a post-tax discounting rate to pre-tax cash flows, the omission of an identified intangible deferred tax liability, are a common cause of material error. Such errors are usually not noticed until the audit phase, where they may necessitate a lot of rework on the whole model.

Process Failures: Where the Modelling Goes Wrong

Coupled with the personal calculation errors, numerous PPA valuation common mistakes are process failures – failures in the planning, coordination and review of the valuation exercise. The process flow below PPA mostly illustrates the main phases of a conventional engagement and the mistakes that can be most probable at each stage. The knowledge of this map can enable professionals to know where to pay attention and where to retreat when they notice red flags.

| Phase | Activity | Key Inputs Required | Typical Errors at This Stage |

| 1 | Deal & Scope Review | SPA, financial statement, management account. | Reading the deal wrongly; disregard to contingent considerations. |

| 2 | Identification of Intangible Asset. | Brand audit, customer contract, IP register. | Mining assets; mixing goodwill and intangibles. |

| 3 | Method Selection per Asset | Royalty databases, industry standards. | Treating all assets in the same way; no reasoning why. |

| 4 | Financial Modelling | Forecasts of revenue, churn rates, discounts. | Circular reasoning in interest rates; disregarding contributory fees. |

| 5 | WACC / WARA Reconciliation | Beta, capital structure, asset risk premia. | WARA significant of WACC; no explanation given. |

| 6 | Goodwill Calculation | Fair value of all liabilities and assets. | Understated intangibles leaving residual goodwill which is too large. |

| 7 | Audit Review & Sign-Off | Workpapers, assumption log, sensitivity tables. | Improperly documented assumptions; lack of sensitivity analysis. |

Among the most repetitive results in post-deal reviews is that they are difficult to rectify errors that were made at earlier stages especially those made in the asset identification and method selection phases. After a model has been constructed on a faulty structure, changes would be superficial as opposed to being structural. The reason behind this is that when you keep advisors who are experienced at the start of an engagement, even before any modelling, is to make sure that the scope is right and the methodology justifiable.

The second flow process below is more direct about PPA modeling error analysis that is, the types of errors that were most frequently detected during quality reviews and the actions that need to be taken to rectify them. Such an organised review is becoming a common practice by accounting firms and teams involved in corporate development as a quality assurance measure prior to a PPA is settled and presented to auditors.

| Error Type | Where It Appears | Financial Impact | How to Correct |

| Incorrect discount rate | Relief-from-Royalty models, MPEEM. | Overstated or understated asset fair value. | Construct WACC afresh; match against WARA. |

| Exaggerated customer loss. | Customer relationship model. | Capitalises the asset value; undervalues amortisation charge. | Take past churn information; make self-adjustments. |

| Omitted contributory asset charges. | MPEEM for intangibles | Value of assets duplicated. | Fairly charge on all contributing assets. |

| Goodwill as a plug figure | Overall PPA schedule | Masks unidentified intangibles; initiates the risk of impairment. | Construct intensive identification of residual calc prior to residual calc. |

| Cases of irregular tax assumptions. | After-tax cash flows, deferred tax. | Mistables pre and post tax returns; misrepresentation of fair value. | Authenticate statutory rate of tax and deductibility of amortisation. |

The common theme in these process failures is the lack of a formal assumption log. A black box model where analysts develop models without providing explanation of the reasons behind each significant assumption (discount rates, growth rates, attrition rates, useful lives), is one that cannot be successfully attacked and reviewed. Auditors are demanding more comprehensive workpapers which document all the material assumptions to a source, and those teams which do not keep the discipline early are usually required to rework much at the start of the audit.

Real-World Cases: What These Mistakes Look Like in Practice

The abstract descriptions of the valuation errors are informative, but it is highly educative when they are based on real-life cases. The following are the cases that show the way PPA valuation common mistakes in practice may manifest themselves and what the outcome may be.

During a mid-market technology acquisition in the United Kingdom, the acquirer finance team put together the PPA in-house and did not hire external valuation experts. The team recognized and appreciated customer relations and software platform of the acquired firm but failed to include the name of the business which was well recognized in the specific market it operated. This omission implied that value that ought to be recognized in identifiable intangible was rather used in goodwill. Three years later, after the acquisition, the business performed poorly and the company performed a good will impairment test and realised a write-down of 18 million. An error analysis of a post-mortem PPA modeling concluded that intangible identification in the first place was not completed materially. Had the trade name been duly recognised and considered in value, the reported goodwill should have been reduced by some 6 million pounds -and the charge of impaired status was disallowed, but not entirely removed.

The second instance is of an acquirer of healthcare services based in the U.S. which had valued the customer relationships of the target based on the MPEEM. The model used the same discount rate, that is, the customer relationship asset, as the WACC of the company obtained 11 percent, without considering the risk premium on this asset that the customer should have. It also did not put in place a contributory asset charge towards the assembled workforce which was an important input to the service delivery. Both of the errors were detected by an external review conducted as a part of the audit process. Following remediation, the fair value of the customer relationships fell by about 22, and a goodwill was increased. The remedy involved having to re-state the original PPA and postponing the filing of the acquisition disclosure note by six weeks. The example is a textbook illustration of the fact that analysis of PPA modeling errors at the review stage as opposed to the preparation stage results in expensive rework and much friction to the reputation.

The WACC-WARA reconciliation problem is shown based on a third case, which is a European consumer goods transaction. Workpapers did not explain or reconcile a gap in valuation between a valuation team that had a WARA of 16.8% and a WACC of 11.2%. At the point when the auditors pointed to the discrepancy, the team failed to offer a rational explanation. The problem up to it was that discount rates had been allocated on an asset-by-asset basis without a systematic framework to provide internally consistent model. The table below shows how a well constructed WARA reconciliation would appear and how each of the various parts would work towards the total return.

| Asset / Component | Weight in Total Value | Required Return | Contribution to WARA |

| Net Working Capital | 12% | 3.5% (risk-free rate) | 0.42% |

| Fixed Assets (PP&E) | 10% | 6.0% | 0.60% |

| Customer Relationships | 18% | 14.0% | 2.52% |

| Technology / IP | 15% | 16.0% | 2.40% |

| Goodwill (residual) | 45% | 18.0% | 8.10% |

| WARA (sum) | 100% | — | 14.04% |

The moral of the three cases is the same they most of the time are not the result of ill intentionality. They are as a result of shortcuts in the processes under review, lack of sufficient investment in the initial steps of the exercise. Those organisations which do not make these errors are the ones where PPA is treated as a substantive exercise of analysis, rather than a compliance requirement to be fulfilled as expediency as possible.

Building Better PPA Practice: Lessons for Professionals

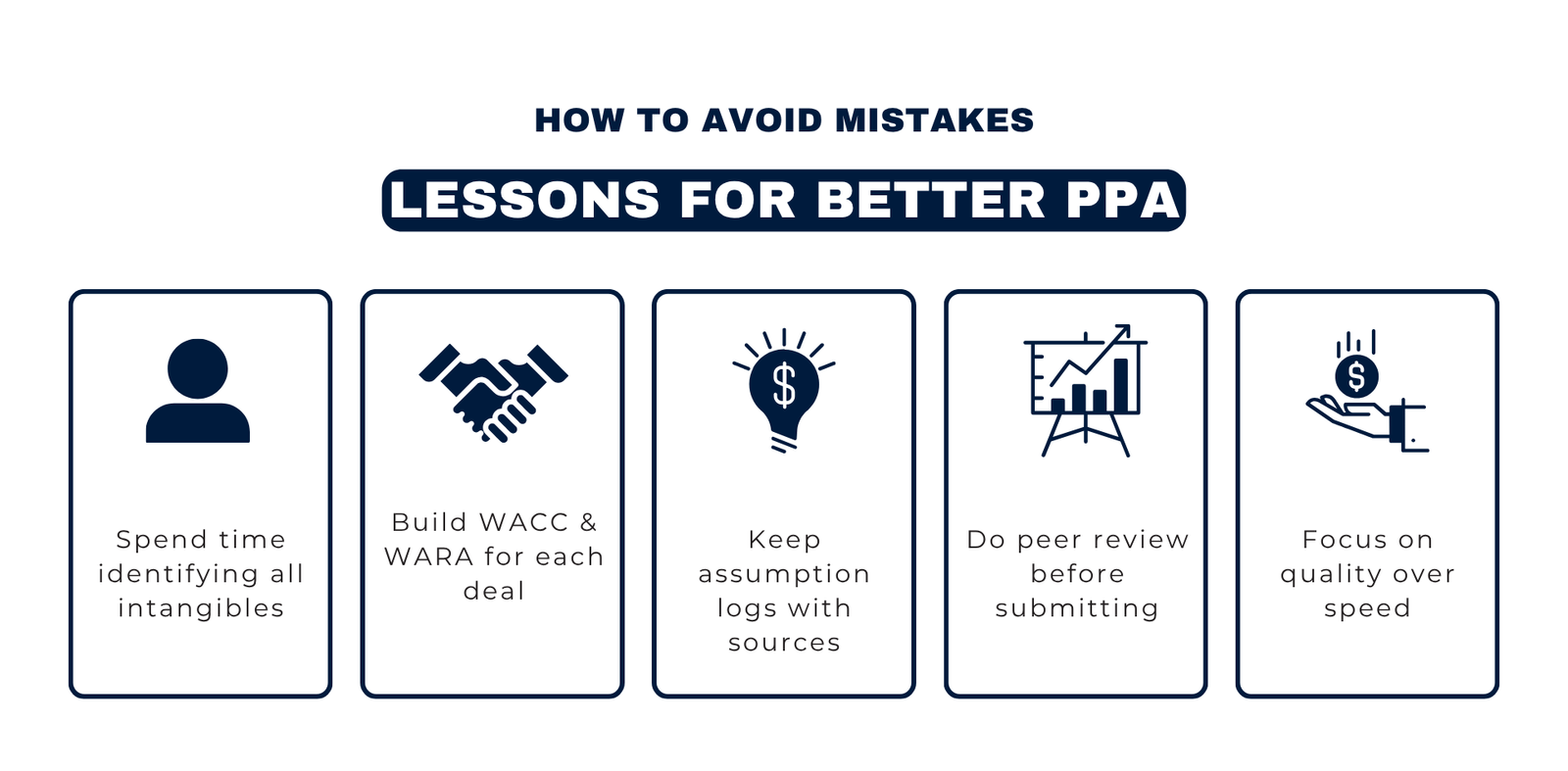

Picture 2 : Lesson for Better PPA

To practitioners who are just developing their competence in this field, the lessons of frequent PPA failures can be applied as a collection of practical disciplines that have a significant positive impact on the quality of work. The first and the most significant one is to invest in the identification stage. The time spent before opening a spreadsheet is to learn more about the business that has been acquired: its customer agreements, technology base, brand positioning, workforce hierarchy, and competitive dynamics. The better you know the business the more complete and confident will be your intangible identification. It is here that the senior advisors waste too much time and reasonably.

The second one is to construct your WACC and WARA on first principles on any engagement. Do not reuse any discount rates of previous transactions without ensuring that the risk profile is similar. Beta data, capital structure review and asset specific risk premium calculation is time-consuming, yet it is on this basis that the entire model is built upon. An advanced auditor or counterparty reviewer will directly review the discount rates, and in case, they cannot be justified, the validity of the whole report is destroyed. Performing a thorough process of PPA modeling error analysis on your own before you submit it, namely, taking a look at the WARA-WACC reconciliation, is a practice that can make the difference between a good practitioner and an average practitioner.

The third lesson is that of documentation discipline. Any assumptions of a PPA model must be derivable: a management interview, historical data extract, industry database, or a published similar transaction. When you are not able to trace to a source of an assumption, it is either unsupported or unverified – and both states give rise to audit risk. When the audit review starts, teams that have an active assumption log all through the engagement, which is updated with incoming information, are much better placed. Lastly, do not wrongly discount the importance of a peer review – before submitting the model, have a colleague not involved in the construction of the model go through the logic, assumptions, and reconciliations before them and they will detect an excessive portion of errors that one-person reviews fail to detect.

Conclusion: Actionable Insights

Purchase price allocation is a field of practice on which the technical knowledge, analytical rigour, and professional judgment need to work together. The errors in PPA valuation recorded in this article, including failure to identify the entire intangibles, the utilization of flawed discount rates, and unreported assumptions are not exception cases. They form the rule in engagements in which the process discipline disaggregates or in which the exercise is seen to be a formality and not a substantive valuation task.

To junior and mid-level professionals, the practical priority goes around the creation of a systematic mental checklist in regard to each PPA engagement. Prior to the modelling process, enquire: Have all intangibles been located? Was the selection of the method justified? Are the discount rates asset specific and reconciled? Does it have verifiable data to support the assumptions? Does it have a definite assumption log? These are the questions that should be asked repeatedly and they will identify most of the findings on the analysis of the error of PPA modeling before it turns into a problem.

In the case of review or supervisory staff, the focus should be to make spaces to promote quality. PPA mistakes are skewed toward those engagements in which the timeline has been shortened, the team over- or under-resource, or the review by seniors was not done sufficiently. Procrastinating the unrealistic deadlines, taking time to have the work reviewed by colleagues and insisting on the completion of a WARA reconciliation prior to signing the work are not the bureaucratic impediments but rather the professional framework that ensures the quality of the work and the credibility of all parties involved.

After all, the professionals who shine in transaction services, and financial reporting are not the fastest ones, but the ones who pose the correct questions, write down their rationale and do not give in to the temptation to use shortcuts. One of the best high-leverage investments you can make during your career is to develop a strict method of PPA valuation error analysis and PPA modeling mistakes at the beginning of your career. These exercises do not get any easier with time, but that is certain that your skill to move through these exercises with a clear and accurate mind will.