Purchase Price Allocation (PPA): From Deal to Disclosure

Navigating the Full Purchase Price Allocation Lifecycle

Introduction to Purchase Price Allocation PPA: From Deal to Disclosure

The act of closing a deal can, in many respects, only be the start. After the ink has dried on an acquisition agreement, the acquiring company must follow a disciplined and time-constrained process: how to allocate the purchase price between identifiable assets that the acquiring company has acquired and identifiable liabilities that the acquiring company has assumed, and ultimately, balancing the results in the financial statements. This is a journey that requires several months; it involves crossing multiple functions within the organisation and is also a subject of scrutiny by the auditors, regulators, and even analysts.

To professionals joining the business of M&A advisory, transaction services, or group reporting, it is critical to learn the timeline of the purchase price allocation process between deal close and audit. The process has a set of requirements, stakeholders, and failure modes in each phase of the process. The repercussions of failing to meet a deadline, classifying an asset incorrectly, or not fully disclosing the allocation can have far-reaching consequences, well beyond the finance team – affecting earnings per share, analyst opinion, and even compliance with regulations.

This article follows the entire PPA lifecycle from the day the transaction closes up to the disclosures of the notes in the audited financial statements. It discusses the main process steps, the rules of measuring the period which have to be followed and which have to be learned the hard way and the rules of measuring the period are the disclosure requirements which are expected to be followed and which have to be learned the hard way. You may be in your first year of working on these engagements, or you are planning to become more of an owner of the process; this guide has been designed in such a way that it is practical in its application.

Purchase Price Allocation (PPA): From Deal to Disclosure | How to Prepare the PPA Process

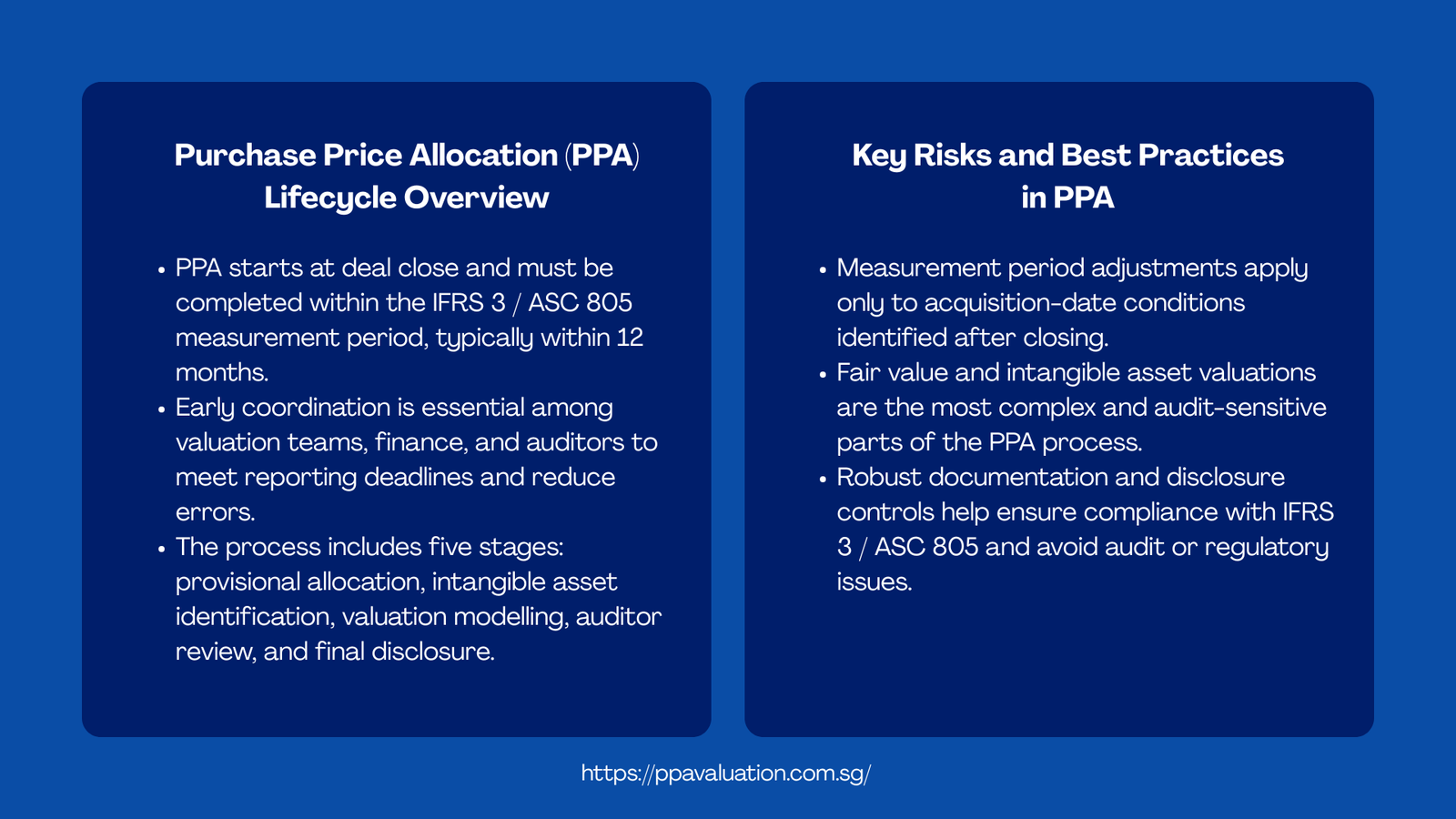

Once an acquisition is closed, a pair of clocks begins to run concurrently. The former is the financial reporting clock: both under the IFRS 3 and the ASC 805, companies are to complete the PPA within the measurement period, which in both cases cannot exceed twelve months since the acquisition date. The second is the interim reporting clock: in the event that the acquisition is within a quarterly or half-year reporting period, then a provisional allocation might need to be reflected in the very next set of interim financial statements, sometimes just a few weeks after close.

This is a dual pressure, such that the groundwork for PPA ought to ideally be laid during the due diligence phase, before close. Practically, lots of acquirers, especially those that are closing their first major transaction, will only start the process after the deal has been closed. This latency decreases the time that is available, and the risk of mistakes is higher. Bringing in a valuation team, putting the key financial and operational data together, and briefing the outside auditors in the weeks leading up to close gives the process a significant head start.

An effective project plan is indisputable. At least, it must identify the lead valuation professional, the internal finance contacts, who will provide the data, the external audit team review milestones, and the reporting dates to which it will adhere, determining when provisional and final figures must be available. In the absence of this structure, engagements are likely to become adrift – and drift in a PPA context equates to a risk to the financial statements. It is not merely a technical issue or even a project management science, but rather an understanding of the purchase price allocation timeline between the close of the deal and the audit.

Table 1: Purchase Price Allocation (PPA) Timeline and Key Post-Acquisition Milestones

| Phase | Typical Timing Post-Close | Key Activities |

|---|---|---|

| Kick-off & Data Gathering |

Week 1–3 |

Involve the valuation team; gather financial information, contracts, and IP registers. |

| Provisional Allocation |

Week 4–8 |

Determine intangibles; prepare first fair value models; interim reporting. |

| Draft Valuation Report |

Week 8–14 |

Full MPEEM / relief-from-royalty model; WARA-WACC reconciliation. |

| Auditor Review — Round 1 |

Week 12–18 |

Complete the report; answer the questions of the first auditor |

| Finalisation & Adjustments |

Month 5–10 |

Include adjustments by including measurement periods; update as necessary. |

| Final PPA & Disclosure |

By Month 12 |

Sign off on final allocation; prepare financial statement note disclosures. |

Note: Timelines vary based on deal complexity, data availability, and reporting deadlines.

Five Key Steps in the Purchase Price Allocation Process from Provisional Allocation to Final Sign-Off

There are five steps in the process of moving a provisional allocation to close to full auditing and disclosure of a PPA. Every step is based on the previous step, and not completing or rushing any step will cause some issues that will have to be resolved with less time in the future.

Step 1 – interim disclosure and provisional allocation. During the time just after close, the acquirer acknowledges a tentative allocation in the financial statements. This is not a market-to-market -it must represent the best available estimates of fair value at the acquisition date using whatever information has been gathered to date. The temporary figures are included in the interim financial statements with a note that it is a provisional allocation that may be adjusted.

Step 2 – Identification and collection of data on intangible assets. Identification of intangible assets that satisfy the separability or contractual-legal requirements of the standard to be used is the heart of any PPA. This involves close scrutiny of customer contracts, technology records, brand registration, employee contracts, and any other value-bearing contract. In a lot of cases, management interviews are required to get to know how these assets can create value and what the competitive advantage of the acquiree is based on.

Step 3- Fair value modelling. After identifying the intangibles, each will have to receive a formal valuation. It is most widely used with the income method (especially the multi-period excess earnings method (MPEEM)) of primary intangibles and the relief-from-royalty method of trade names. The models should be constructed based on assumptions about the market participants that should be supported by observable data, where feasible, and tested with regard to internal consistency through a WARA-WACC reconciliation. It is the most technically challenging step and the one that is most prone to potentially attract audit challenge.

Step 4 – Auditor involvement and cyclic review. The draft valuation report is sent out to the external auditors, who will normally send their own valuation experts to look through the methodologies and assumptions. This is not a one-step process; it consists of a series of questions, answers, and maybe even model enhancements. It is significant to record in a clear manner every change of assumptions that will be made in the course of this procedure, and the rationale for it.

Step 5 – Final allocation, end of measuring period, and disclosure. When the auditors have attested on the allocation, the final figures are locked, and the figures are disclosed in the annual financial statements. In case any adjustments have been made in the measurement period since the provisional figures were published, then such must be disclosed with an explanation of what new information led to such disclosure. The period of measurement ends when all the information is received or twelve months, whichever is earlier. It is an official process, and not a passive consequence.

Purchase Price Allocation (PPA): From Deal to Disclosure | Measurement Period

One of the most misconstrued parts of purchase accounting is the measurement period. Both IFRS 3 and ASC 805 provide that it is the window that during which provisional fair value estimates may be retrospectively adjusted; in other words, that in the event of new information being discovered about circumstances that existed at the date of acquisition, the opening balance sheet may be restated. It is a very limited and particular provision, and is often more broadly applied than is allowed by the standards.

To manage purchase price allocation in the measurement period, the difference between the two kinds of post-close information is required. The former is data on conditions existing on the acquisition date but not on the provisional allocation date – this qualifies to have a retrospective measurement period adjustment. The second one is news of events or developments that arose since the date of acquisition- this does not qualify and should be recognised in the post-acquisition earnings. The two are often confused and become the source of audit disagreements and mistakes in the financial statements in more severe cases.

An example case in point: in case an acquirer learns, three months after close, that a contract with a customer, assumed to be in good standing, was actually in dispute at the acquisition date, the fair value of the associated customer intangible may need to be revised downwards, through a measurement period adjustment. In comparison, an impairment should be recognised as a post-acquisition expense – rather than as a retroactive change to the PPA, in the event that a key customer decides to terminate their contract six months after the acquisition date due to a post-close service failure.

The administrative costs of administering purchase price allocation at the measurement period are high. All temporary figures should be monitored, and each new piece of information should be evaluated to determine whether it could be a measurement period adjustment or not. Many companies that fail to ensure good internal controls of this process are often found not capable of clearly identifying provisional as final figures at year-end, which puts unnecessary pressure on the audit.

Table 2: Purchase Price Allocation Measurement Period Adjustments — Qualifying vs Non-Qualifying Scenarios

| Scenario | Qualifies as Measurement Period Adjustment? | Accounting Treatment |

|---|---|---|

| New data relating to a liability that was in existence as of the acquisition date. |

Yes |

Post-adjustment of tentative PPA; re-state comparatives. |

| Termination of the customer contract in case of failure of the service it provides after the contract is closed. |

No |

Identify impairment or loss in the P&L of the post-acquisition. |

| Re-determined tax assessment on the pre-acquisition period. |

Yes |

Alter deferred tax liabilities in the provisional balance sheet. |

| Reduction in the market value of the property acquired after close. |

No |

Determine impairment under the applicable standard post-acquisition. |

| Recalculated appraisal of PP&E based on the condition at the date of acquisition. |

Yes |

Adjust the fair value of PP&E; adjust goodwill accordingly. |

| A new business controversy that occurs after the acquisition date. |

No |

Recognise provision in post-acquisition financial statements. |

Note: Assessment requires professional judgment and reference to IFRS 3.45–49 or ASC 805-10-25-13 through 25-19.

PPA Disclosure Requirements Under IFRS 3 and ASC 805 for Financial Statements

The requirements of the disclosure under the IFRS 3 and the ASC 805 are prescriptive and detailed. To the professionals who prepare or review the PPA note in the financial statements, knowing what to disclose and how to present it in a clear manner is a core competency. The disclosure of the economic substance of the transaction in a form that can be used by analysts and investors is not only the required form as per the regulation, but also conveys the economic substance of the transaction.

A step-by-step guide to the disclosure of the PPA financial statements should start with the qualitative narrative: an account of the company that acquires, the date of acquisition, the rationale of the acquisition, and the percentage of voting equity that is acquired. This is preceded by the quantitative disclosure of the consideration transferred – including cash, equity issued, and contingent consideration – and the fair values of each category of recognised assets and liabilities. The goodwill balance and the aspects of it (including workforce, synergies, or market position) need to be explained as opposed to being stated.

The disclosure should also discuss the adjustment of the measurement period, provided that there were adjustments during the period. With every adjustment, standard mandates that the amount of the adjustment and the purpose of the adjustment are presented, that is, what new information has been obtained. Such specificity can be quite startling to practitioners not involved in disclosures previously. Any vagueness, like the one in revised assumptions, cannot suffice; the news must be disclosed to state what assumption has been revised and why.

This will also include following a step-by-step guide on PPA financial statement disclosure, which also implies that the revenue and profit disclosure requirement under IFRS 3 would also be attended.B64(q): the amounts of revenue and profit or loss of the acquiree included in the consolidated income statement (at the time of the acquisition) must be disclosed. This additional disclosure is often not disclosed, or is improperly disclosed by first-year practitioners, and is a frequent area of auditor questioning.

Table 3: Key Purchase Price Allocation Disclosure Requirements Under IFRS 3 and ASC 805

| Disclosure Item | IFRS 3 Reference | ASC 805 Reference | Common Gap in Practice |

|---|---|---|---|

| Acquiree description and strategic justification. |

B64(a) |

805-10-50-2(a) | Too short; does not have an economic background. |

| Consideration conveyed (cash, equity, contingent) |

B64(f) |

805-10-50-2(d) | Contingent consideration that is not reported separately. |

| Fair values of every type of asset and liability. |

B64(i) |

805-10-50-2(h) | Insufficient granularity on intangible classes |

| Goodwill and description of contributing factors in a qualitative manner. |

B64(e) |

805-10-50-2(c) | Language of boilerplate employed; no explanation of the deal. |

| Adjustments in the measurement period (where applicable) |

B67 |

805-10-50-5A | The description of the nature of new information is not described adequately. |

| Revenue and profit of the acquiree after close; hypothetical after full year. |

B64(q) |

805-10-50-2(h)(3) | Frequently left out or approximated without a specific procedure. |

Note: Both standards require additional disclosures for individually material acquisitions and for contingent consideration remeasurement.

Real-World Purchase Price Allocation Case Studies Across the Full PPA Lifecycle

The entire curve between deal and disclosure hardly ever flows smoothly and the most valuable professional development is often what happens on actual engagements – and why. The following are scenarios that depict common challenges that are faced at all stages of the PPA lifecycle.

Case A – The Compressed Interim Reporting Deadlines: A European industrial conglomerate was acquiring a mid-sized machinery manufacturing company at the end of September, just a few weeks before the 30 September half-year reporting date of the acquiring group. The finance department had assumed that the PPA would only be provisional and that the interim note would merely say that the allocation was provisional. However, the external auditor of the group came to the conclusion that the provisional figures would require more than a placebo and that the major categories of assets would require specific fair value estimates, even though it might be only a placebo. The engagement team had under ten days to come up with indicative valuations of property, plant, and equipment, customer relationships, and order backlog. The moral: acquisitions that are near reporting dates should have close emergency PPA resourcing plans agreed with auditors prior to close, rather than after close.

Case B – A Measurement Period Adjustment Has Been Made Incorrectly: In the year following an acquisition in the North American healthcare sector, the finance department of the acquirer found out that the revenue of the acquired business that was received during the year in question was lower than the projections that had been used during the PPA. In an attempt to avoid an impairment charge, the team offered a change in the measurement period to lower the fair value of the customer relationship intangible. The auditors disallowed this because the underperformance of the revenue was a post-acquisition event and did not indicate conditions that existed at the acquisition date. This adjustment was not allowed, and the impairment was charged on the income statement. The PPA report was evaluated for quality. This case highlights one obvious failure to perceive the difference at the core of handling purchase price allocation during the measurement period: the measurement period is no such thing as a remedy for poor deal economics.

Case C — Inadequate Disclosure Attracting Regulatory Comment: A listed Australian consumer group had completed a material acquisition and prepared the PPA note, in large part by adapting a template out of a prior year disclosure. The intangible assets identified were recognised, but the hypothetical full-year revenue and profit disclosure were not provided as required, and the description of the goodwill was generic. The securities regulator has sent out a comment letter because of non-compliance with the revenue disclosure requirements and inadequacy of the goodwill qualitative description. The finance department was forced to prepare additional disclosures, and communications with the regulator would require the team to dedicate a lot of time to the correspondence. The root cause of failure was very simple: no one had read the disclosure requirements carefully and ascertained whether what had actually been prepared met the requirements. Both gaps would have been identified prior to filing by a simple compliance checklist, which is used as a final review step.

Purchase Price Allocation (PPA): From Deal to Disclosure | Best Practices

The path between deal and audit sign-off of a purchase price allocation is long, complex, and has more significant consequences than many professionals first realize when they first encounter it. Any mistake in one of these dimensions can cause a problem that would affect all the others.

The greatest practice lesson is that the schedule of the purchase price allocation between the deal close and the audit requires early action. Waiting until the deal has closed, then involving the valuation team, identifying the intangible assets, or briefing the auditors are structural disadvantages that cannot be completely recovered. Those acquirers and advisers who deliver high-quality PPAs are always those who consider the process to start during due diligence and not after close.

The discipline that guided the measurement period entails thorough documentation and a clear picture of what is eligible to be adjusted retroactively. Teams that have a continuous record of tentative assumptions, which keep their record of every bit of new information that arrives post-close, and which formally make an evaluation as to whether each item meets the criteria of the measurement period, will be much better placed at the end of the year than teams that only attempt to reconstruct the timeline in retrospect and under audit pressure.

The best tool for disclosure is a compliance checklist, which is directly based on the standard in question – IFRS 3, B64 to B67, or ASC 805-10-50 subtopic – compared line by line with the draft note. It is not an advanced exercise, but it is a good one, and the number of occasions on which gaps in material disclosure arise in practice points to the conclusion that it is not being done by many teams. The step-by-step guide to the PPA financial statement disclosure is, in essence, concerning the reading of the standard and matching the output to the requirements of the standard.

Lastly, to junior and mid-level professionals interested in developing real competence in this area, the best investment would be the involvement in the entire process, not just the valuation models. Having a 360-degree command of the subject, which cannot be replicated with purely technical training, understanding of how the numbers flow out of the valuation report and into the provisional balance sheet, how they are adjusted during the measurement period, and how they are ultimately reported in the audited financials. The most valued professionals in this field are those who are able to speak fluently through all three stages of the deal, measurement, and disclosure.