What Creates the Highest PPA Valuation Risk?

Understanding What Creates the Highest PPA Valuation Risk?

With each business acquisition, comes a time of reckoning: After a deal closes, accountants and valuation experts are tasked with converting a negotiated purchase price into a formal, set of numbers on the balance sheet. This process is called IFRS 3 purchase price allocation and demands management identify and measure each asset and liability acquired at fair value, whereupon any surplus goodwill. Knowing how to value PPA risk is crucial for junior and mid-level finance team members as it can impact financial statements, lead to audit findings and affect a company’s credibility with investors, potentially years after the investment has been signed and announced. Knowing where valuation risk lies is a factor that will distinguish you when it comes to interviews or the day-to-day work of an accountant in a transaction advisory or corporate accounting role. This article outlines and addresses how PPA valuation risk is defined, where it originates from and how professionals can navigate this type of valuation risk with confidence and discipline, offering practical steps and real-world examples that can be applied to a real deal (and not just in theory).

What Is IFRS 3 Purchase Price Allocation and Why Does It Create Valuation Risk?

IFRS 3 Purchase price allocation is the accounting process which records a business combination. Under the standard, the amounts at which the identifiable assets acquired by the acquirer and the liabilities assumed by the acquirer are recognized are their acquisition-date fair values, except for goodwill, which is the amount by which the acquisition-date fair value of the net assets acquired exceeds the total consideration transferred. In theory, it’s simple; in practice, it’s more complicated because of the value of things that are rarely freely traded in the open market, like customer relationships, brand names, in-process research and development, non-compete agreements and assembled workforces. All of these involve assumptions regarding future cash flows, discount rates, useful lives, attrition rates and market comparisons, which are inherently uncertain at the time of acquisition, and all of which require a fair value allocation. A business combination requires the acquirer to examine what is inside the target and put a separate value on the target’s intangible assets, which have not been sold or traded separately before the transaction. This is why purchase price allocation is a more challenging part of accounting for many finance graduates than other parts: it requires them to be comfortable with a spreadsheet model of the business, but also requires them to be equally at ease in a conversation with the operational management about how the business actually generates revenue, which requires knowledge of accounting standards and an understanding of corporate finance theory.

The danger is just because these valuations rely on judgment instead of seen prices. V2 is not limited to providing a single valuation. It is not possible for value professionals to reach a single valuation when using the same intangible asset; the method, discount rate, or growth assumption in a cash flow model may vary. Aggressive or poorly documented judgments, or judgments that differ from business operations, increase the valuation risk associated with PPA. For years after the transaction, over- or under-allocating a purchase price to identifiable intangible assets can have a significant adverse effect on a company’s financial position, and this has attracted the attention of regulators and auditors. The significance is that the allocation of intangible assets has a direct impact on the earnings that a company reports in all future periods because these assets are usually amortized over the useful lives, while goodwill is not amortized but is tested for impairment once a year. Senior finance leaders tend to be much more careful than they may be led to believe by the technical nature of the exercise about which they are being asked to approve an allocation in a hurry or in an incomplete manner—an allocation that, for a number of years after the acquisition, will impact key performance indicators like return on assets, EBITDA margins, and debt covenant calculations.

Which Factors Create the Highest PPA Valuation Risk?

The purchase price allocation contains a number of uncertainty elements, but they are not all of the same level. The fair value allocation of tangible assets, such as land, buildings, and equipment, is often fairly easily defendable as there are readily available market prices or methods of appraisal, and there are relatively few disputes. This isn’t the case with intangible assets and contingent liabilities. The income-based models for customer relationships, technology and brand value are based on management’s forecasts which are naturally optimistic and hard to verify independently. Then there is contingent consideration, earn-outs and pending litigation, which further complicates things because the value of the consideration is uncertain and it must be estimated at the date of the acquisition, typically by relying on some probability-weighted scenarios or option-pricing models that few younger professionals are likely to see outside of the deal team. Assembled workforce value and some of the acquired research projects are also somewhat murky: Accounting standards place restrictions on what can be separately recognized, and part of the analytical question is determining which projects, if any, are worthy of being recognized as a separate asset in the first place.

This uncertainty is further complicated by a number of structural factors. Working under urgent deadlines with valuers means less time to collect evidence, transactions involving private targets are often more precariously equipped with historical financial records, and cross-border transactions present additional currency, regulatory and market-comparable problems which don’t arise on domestic transactions. The table below is a helpful summary of where PPA valuation risk is likely to be focused as a result of common trends that have been seen across the acquisition landscape across different sectors, including technology, manufacturing, and services. The industry also has an influence: technological or pharmaceutical transactions are more likely to feature intangible assets, and thus higher risk overall, while companies in sectors like logistics or industrials have a higher proportion of value in tangible assets, which are easier to verify. Knowing this, professionals can determine, even before a valuation is drafted, about how much attention a particular transaction will receive from auditors.

Table 1: Common Drivers of PPA Valuation Risk

| Risk Driver | Typical Cause | Relative Risk Level |

|---|---|---|

| Intangible assets (brand, technology, customer lists) | Reliance on forecasts and unobservable inputs | High |

| Contingent consideration / earn-outs | Uncertain future performance outcomes | High |

| In-process R&D | Early-stage projects with uncertain success rates | High |

| Property, plant, and equipment | Reliance on appraisals, but generally observable | Medium |

| Inventory and receivables | Short measurement period, more objective data | Low |

The table indicates that the highest valuation risk for PPA lies in the unobserved and forecast dependent inputs. That is why auditors and regulators are reviewing intangible asset valuations and contingent consideration at a far greater level of depth than they review inventory or receivables, where you can typically go to existing records to verify the value. It is also a good practice to ask when considering a draft allocation whether the allocation is selected based on a forecast or market price, because these items tend to generate audit questions and are the most likely to be double checked before the file is sent to the client. This is the same lens to use for transaction advisory or valuation positions in interviews as candidates who can articulate that intangible assets are riskier than inventory will impress.

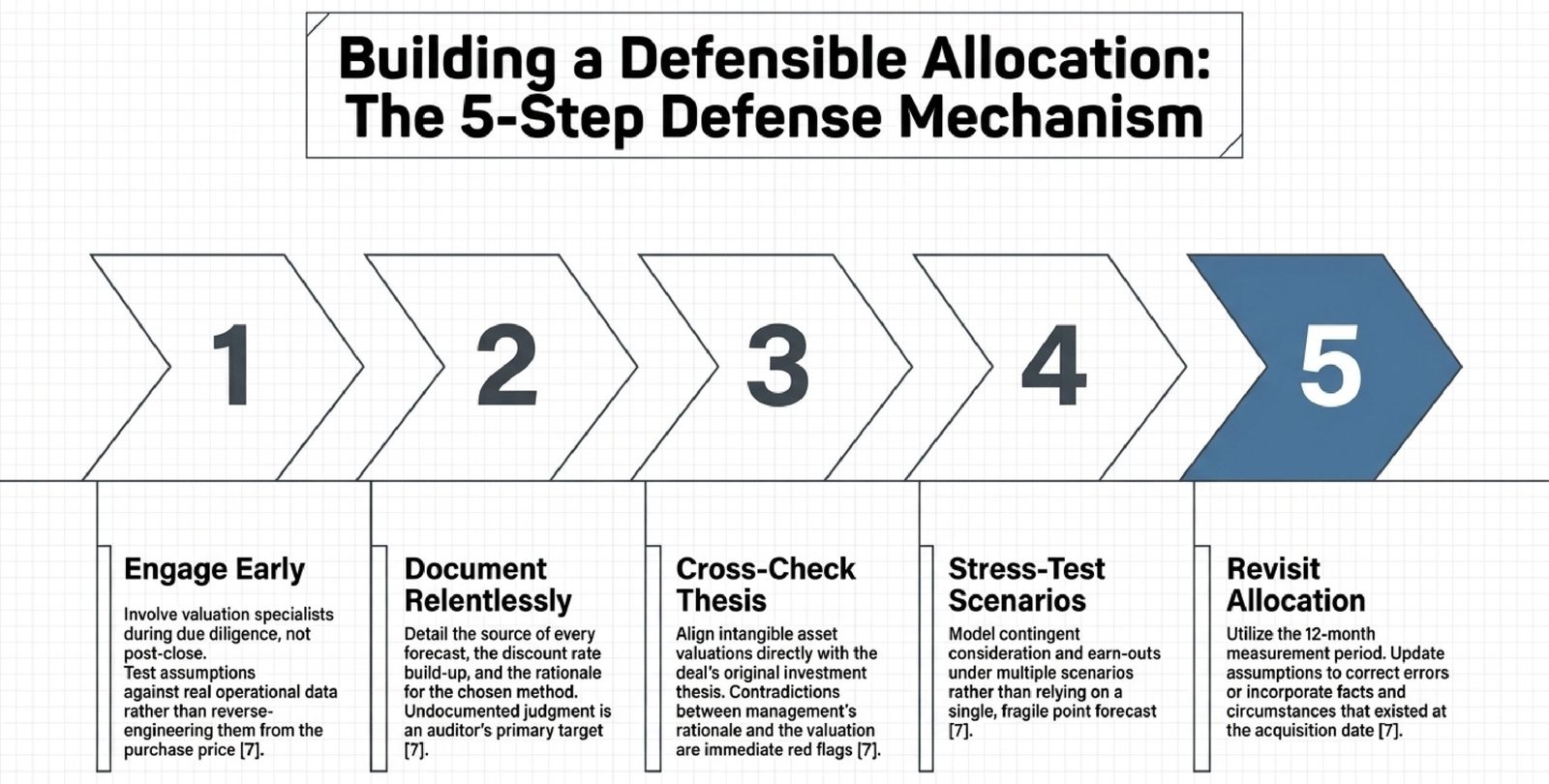

What Are Five Key Steps to Reduce Fair Value Allocation Risk?

Risk can be reduced by professionals on purchase price allocation by following a disciplined process instead of a purely mechanical valuation process. The five steps outlined below come from the common practice of valuation and audit teams to ensure an allocation is defensible from the time of its inception through the final audit. All of these steps don’t need to be advanced technical steps as such, but they do need to be steps that are taken in a disciplined manner and as part of early planning and asking uncomfortable questions before a number is committed to the financial statements.

Firstly, bring in valuation experts early, preferably during the due diligence phase; too late to sign and usually adds extra pressure and shortens the process, to accept the first reasonable figure suggested. Second, you’ll need to record every assumption that you make to reach the final value. They must know where the forecasts came from, how to calculate the discount rate, what the reasons are for choosing a specific valuation method, and so on; undocumented judgment is the first the auditors will look at and the most difficult to build up, a month or two later. Third, compare the valuation of intangible assets with the deal itself investment thesis – if a company is being acquired for its customers, for instance, then intangible asset valuation should include some value in the customer, not all in goodwill. Fourth, calculate contingent consideration and earn-out estimates based on a variety of potential scenarios rather than a single point estimate; contingent consideration and earn-outs are among the least observable and most challenged components in any audit or dispute with the sellers. Fifth, reassess the allocation in advance of the measurement period (generally within 12 months of the acquisition date) to reflect any changes in the facts and circumstances that existed at the acquisition date, based on newly-available information, not on what actually transpired later in the measurement period. Combined, these five steps move the allocation from a reactive exercise (where numbers are invented to meet a filing deadline) toward a proactive one (where the allocation is truly in line with the economics of the transaction and stands up to any auditor, regulatory or investor challenge).

What Real-World Examples Show About PPA Valuation Risk?

Think of a midsize software firm that’s been bought by a bigger tech firm. In the purchase price allocation, the valuation team for the acquirer valued a large portion of the purchase price on a proprietary software platform using a relief from royalty approach with a assumed royalty rate taken from an unrelated industry source and not based on the company’s own royalty history. The assumption was not without cause as the benchmark rates were sourced from a well-known third party data source, but no one on the deal team took the time to ensure that these benchmarks aligned with the target’s business model. Later, auditors compared the assumed royalty rate to the actual royalty rates the target had negotiated with third parties, and found it to be significantly too high, which led to a restatement of the value of the intangible asset to goodwill and the company’s audit committee had to account for that difference. The example below is an example of this PPA valuation risk – how the assumption may appear reasonable individually but may not consider the economics of the business being acquired. It also emphasizes a key lesson for junior analysts—just because they draw a benchmark from a database doesn’t mean they should assume it is the benchmark they should apply to the target’s own contracts, pricing history and competitive position—the entire purpose of a fair value exercise is to reflect the actual asset being valued, not an industry average. This type of sanity check saves a lot of time over a later restatement, but often is the thing that is overlooked when a deal team is in a hurry to close a deal.

The second example is from a manufacturing acquisition where the purchase price allocation was understated by the failure to recognize an environmental remediation liability due to an old manufacturing facility. The original valuation was based on a preliminary environmental assessment as much of the deal was closed prior to the time needed for a full site survey. The estimate was significantly raised after contamination testing took place during the measurement period and the increase was material enough to cause the allocation of the liabilities and goodwill to change. The revision was made prior to the end of the measurement period, and in that sense, was not an error, but it still had to be disclosed, reviewed internally several times and caused a delay of a few weeks for the finalization of the accounts. In both cases, PPA valuation risk is largely a consequence of incomplete information or overly compressed time horizons or assumptions that weren’t stress-tested with the target’s actual operating history prior to capturing them in the financial statements. The lesson for any professionals who are looking at similar deals is to keep in mind that any valuation based on an initial assessment is provisional by definition, and to make sure it’s marked as such in the working papers, and allow time before the measurement period closes for the valuation to be revisited when more information becomes available, but not just because the deadline has passed.

What Are the Benefits and Challenges of Managing PPA Valuation Risk?

An effective FA includes more than meeting compliance requirements. Provides investors with a better understanding of the items actually purchased, distinguishing the value of identifiable assets that are typically amortizable from the goodwill, which will impact future earnings in amortization and impairment tests for many years. It also enhances the credibility of management, which indicates that they knew the business they acquired rather than justifying the price paid to the board or to shareholders. It is important for finance professionals early in their career to gain experience in this process, as it teaches them the skills they need in financial modeling, negotiation, and collaborating cross-functionally with legal, tax and operational teams, and it is one of the quickest ways to get exposure to senior stakeholders on a live deal. A clear allocation can also make transactions easier in the future, as it will be much easier to answer due diligence questions if the acquired business is subsequently sold, restructured or offered for collateral in financing.

The difficulties, however, are great. Purchase price allocations are usually done with a narrow time window, with integration teams often working together to integrate the operations, meaning that a time period too short for a reliable fair value allocation. Because of the limited data in the private segment, especially for private targets, where valuation teams have to rely on management representations, which may become overly optimistic in the future. Additionally, auditors and regulators are now more challenging assumptions and documentation than ever before, even when an otherwise technically sound valuation is done, and documentation supporting the assumptions is lacking. One of the more practical challenges that professionals have to overcome when dealing with PPA valuation risk on a live transaction is balancing these pressures against accuracy and by this point it is usually only through experience that this skill will get better. The added complication from cross-border transactions is local regulatory requirements, currency translation, and the fact that similar market data availability with the target are all factors that can be used to distort the reliability of a fair value allocation, especially when the target is operating in an unfamiliar market to the acquirer’s finance team. Being aware of these issues early and having a plan in place before they arise in the deal timetable is often the difference between a smooth purchase price allocation and a purchase price allocation that continues to drag on for months after closing.

Conclusion

The highest risk of valuation relates to PPA valuation where judgement is applied instead of observable market data, notably for intangible assets, contingent consideration or any estimate based on management’s own forecasts. The practical lesson for professionals seeking to develop a career in valuation, accounting and/or M&A advisory is to think of each assumption in an IFRS 3 purchase price allocation as one that needs to be sourced, documented and justified, rather than merely assumed. Don’t think of the engagement of specialists early, stress-testing forecasts, cross-checking valuations to the investment thesis of the deal, and reaping the allocation before the measurement period is over as bureaucratic niceties—they are the elements that can make the difference between a defensible fair value allocation and one that comes undone under audit pressure months or years later. Valuation, accounting and transaction advisory are disciplines that are easy to master early, and in which it’s easy to see how forecasts replace reality – a skill that will come in handy to anyone in finance beyond a single deal. The experts who can confidently tell you why a number was selected, rather than just how they’ve calculated it, are the ones that will be trusted with larger and more delicate transactions, across all fields and borders.