How Does IFRS 3 Impact Purchase Price Allocation Requirements?

IFRS 3 Business Combinations sets out the requirements for the recognition and measurement of assets, liabilities and goodwill at the date of acquisition of a business. Under IFRS 3, the purchase price allocation calls for the allocation of acquisition cost to the identifiable assets and liabilities of the business at fair value and the remainder as goodwill. This process is essential for the accuracy of financial reports, compliance with taxes and making strategic decisions. Whilst these assets may be intangible, they can also be important and have been acquired at a high price, with organisations needing to identify them, put them to value and value them in accordance with IFRS 3 guidance.

Key Takeaways

- According to IFRS 3, the fair value of all identifiable assets and liabilities must be measured at the date of acquisition.

- Only those assets which can be recognized under the recognition criteria are included in the definition of intangible assets and must be measured in accordance with the income, market or cost approaches.

- Goodwill comes into existence only when all assets and liabilities identified have been valued at fair value.

- The total purchase price and allocation is impacted by contingent consideration and acquisition costs.

-

How Does IFRS 3 PPA Requirements?

Introduction to How Does IFRS 3 Impact Purchase Price Allocation Requirements?

The actual cost of business assets purchased and liabilities assumed is much more complicated than considering just the transaction price when organizations acquire a business. IFRS 3 Business Combinations must be based on a strict process of purchase price allocation that allocates the purchase price to identifiable assets and liabilities acquired in the acquisition at their fair value on the date of acquisition. In most cases, the bulk of the value of an acquisition is in the intangible assets of the company, such as its customer base, acquired over many years, its brand value, recognized throughout markets, its proprietary technology, and its workforce capabilities. The finance problem is how much of the buying price should be attributed to each of these assets. This allocation has an impact on the initial balance sheet, as well as subsequent goodwill impairment testing, depreciation and amortization, calculation of tax and reported profitability. The valuation of intangible assets, as covered by IFRS 3, is therefore one of the most important and controversial aspects of the merger and acquisition accounting. This article delves into the implications for allocation mandates, reviews the identification and valuation process, highlights some of the common issues in implementing IFRS 3 and offers a few ideas for handling this crucial compliance arena.

What Is IFRS 3 and How Does It Define Purchase Price Allocation?

Business Combinations is an International Financial Reporting Standard (IFRS) that applies to the accounting of business combinations by acquirers. A business combination is defined as a business combination under IFRS 3 to be an event in which an entity acquires control of one or more businesses, usually by acquiring them. The essential element is that assets acquired, liabilities assumed and goodwill derived from the acquisition be recognized in accordance with the acquisition method. The purchase price allocation in the IFRS 3 framework starts with determining the total consideration transferred, including the fair value of assets transferred, liabilities assumed, equity instruments issued and contingent consideration. This entire consideration is then allocated, on a systematic basis, to the identifiable assets acquired and assumed obligations, respectively, at their respective fair values. The amount of goodwill (or a bargain purchase gain if the total consideration is less) is the difference between the total consideration and what is defined as the sum of the fair value of identifiable net assets. In accordance with IFRS 3, identifiable assets are defined as assets that are separable or result from contractual rights arising from the business combination and identifiable liabilities are those that are contractual or constructive obligations arising from the business combination.

The importance of proper allocation of purchase price goes beyond the mechanics of accounting. The allocation has financial statement impacts that extend over several years as it results in a direct impact on the value of intangible assets, future amortization expense, tax deductions and goodwill impairment charges. However, by conservatively allocating values for the intangible assets, the amount allocated to goodwill is overstated, becoming an impairment charge if the acquisition underperforms. On the other hand, heavy charges in the current period against identifiable intangibles creates greater amortization expense in the period of acquisition, which lowers the immediate profitability, but allows for the tax deduction. Such allocations are closely monitored by the regulators, auditors and tax authorities. Companies need to provide documentation of methodology, valuation assumptions and supporting analyses to support their arguments. This is where IFRS 3 PPA valuation services come in handy – the valuation expert uses special techniques and data to assist with fair value measurements that will pass the audit and regulatory scrutiny.

Which Assets Require Valuation Under Purchase Price Allocation?

Not all assets need to be valued in IFRS 3, but only those that are identifiable as assets and identifiable as liabilities. Tangible assets, such as land, buildings, machinery and inventory, generally have readily discernible market values and are fairly easy to measure. But intangible assets are the most complicated to value, and also are the area where purchase price allocation under IFRS 3 is most complex. Intangible assets that can be identified and have a useful life of over one year are recognized under IFRS 3, such as: customer relationships and contracts, trademarks and brand names, patents and proprietary technology, software and databases, contractual rights (licenses, permits, supply agreements), workforce relationships. All these should be recognized in accordance with the IFRS 3 recognition criteria. Some intangibles are separable, meaning that they can be sold or licensed separately; others from contractual or legal rights. Any asset not qualifying for this is not recorded separately, but rather added to goodwill. The real-world implication of the IFRS 3 intangible asset valuation is that the first step is to identify intangible assets that can be recognized, which is a judgment call and sometimes a game of negotiation between the parties involved, namely the acquirer, the professionals and the auditors.

A comparison table shows how the various asset categories in the purchase price allocation relate to the valuation methodology. Customer relationships, for example, can be recognized as they can be separated by contractual evidence (customer lists, retention history); the valuation of a relationship usually is the excess earnings method (net cash flows from the relationship over the expected life of the relationship). Although often created within the company and not separable, trademarks and brands are considered to be contractual or legal rights that are recognized in a business combination, typically valued using the relief from royalty method, which estimates the fair value of the trademark or brand as the present value of the royalties saved by being the owner of the trademark or the brand. The income approach to value technology assets (patents or software) is based on capitalizing the incremental cash flows they generate. Goodwill occurs when all these identifiable assets and liabilities are measured, and it refers to the value resulting from synergies, market position, assembled workforce and other factors that don’t qualify as separately identified intangible assets. This layered approach will ensure the purchase price allocation of IFRS 3 to be systematic, defensible and compliant.

Table 1: Asset Category – How Does IFRS 3 PPA Requirements?

| Asset Category | Recognition Criteria | Valuation Method |

| Customer Relationships | Identifiable, separable | Excess earnings method |

| Trademarks & Brands | Identifiable, separable | Relief from royalty |

| Technology | Separable, patented | Income approach |

What Are the Key Challenges in IFRS 3 PPA Implementation?

There are many practical and technical issues to be solved by organisations that have adopted the IFRS 3.5 consensus regarding purchase price allocation. First, there is a lot of time pressure. Business combinations are usually closed following several months of due diligence and negotiation and the acquirer must complete the PPA within one year of acquisition (the measurement period). In this period, they need to collect information, hire experts to value the business, and conduct in-depth studies, whilst at the same time integrating the acquired business operation into the existing business. Secondly, information is often scarce in the process of valuing IFRS 3 intangible assets. Forecasts of future cash flows are necessary to measure a business acquired on a fair value basis, but if the acquired business has limited or unreliable financial history, and the projections are inherently uncertain. There may be gaps in the target company’s customer retention, churn, and margin characteristics. Proprietary technology’s commercial potential may not be quantifiable until post-acquisition use. Thirdly, the measurement and valuation of some intangibles are subject to judgment calls that are inherently “controversial. For example, the value of an acquired company’s workforce and its skill set is typically not separately identifiable, although in some cases (such as service companies) the value of workforce is significant and defensible. It can be difficult to distinguish between separable and contractual, and it is easy to see how there can be differing views between management, auditors and valuers as to what is separable from what is contractual.

Fourth, the basis for the adjustments to valuation models are sometimes shifting and hard to justify in the market and economy. The application of the discount rates, terminal growth rates and revenue multiples has a material impact on IFRS 3 intangible asset valuation results. Should assumptions be changed if there is a significant change in market conditions after the date of the acquisition but prior to the end of the measurement period? Fifth, multi-year amortization of intangibles makes accounting for them complex over time. A compliance burden is created by the need to test for impairment of indefinite-life intangibles, such as some trademarks, as per IAS 36, every year. Amortization of finite-life intangibles needs to be done in a consistent manner to their useful lives, and any error in useful life equates to years of incorrect expense recognition. Last but not least, audits and taxes increase the risk of PPA. Aggressive valuations are met by auditors, and tax authorities around the world are critical of the allocation to ensure that transfer pricing principles are followed and base erosion is avoided. The professionals should therefore strike the right balance while dealing with IFRS 3 PPA valuation services, between the comprehensiveness, defensibility and pragmatic aspects of the IFRS 3 PPA valuation.

How Does IFRS 3 Impact Intangible Asset Recognition and Measurement?

IFRS 3 provides a complete reworking of the principles for recognizing intangible assets in contrast to the organic development or internal creation of assets. The IAS 38 Intangible Assets prohibits recording internally generated intangible assets as assets (e.g., customer relationships, brands). IFRS 3 does allow intangible assets to be recognized in a business combination, even though they are not recognized if they are generated by the acquirer. The recognition difference is quite significant. If a company acquires a competitor, they can also value the target’s brand, customer base and technology as intangible assets, where if the assets are created within the company, they can’t. This results in an apparent paradox – the more assets are recognized as a result of the acquisition accounting than would be with the organic growth of the business. The reason is because the IFRS 3 intangible asset valuation under a business combination has observable market-based data as its foundation (purchase price) and fair value measurement at a particular transaction date. The cost of acquisition is a market-tested basis for recognizing and valuing the intangibles not recognized on the basis of internal generation. In addition, IFRS 3 requires that acquired intangible assets be identifiable which generally means that they are separable (can be sold, licensed or transferred) or are contractual or legal rights. This identification criterion also adds rigor to the identification process as only those intangibles that are actually transferable and legally defensible are recognized.

The IFRS 3 Transition Working Group makes several changes to the way fair value is measured under IFRS 3, including specifying that fair value be measured at the date of acquisition, and using valuation techniques that reflect the cost of an asset to market participants. The income approach is often used in the IFRS 3 accounting for the intangible asset valuation, and it is the present value of future cash flows associated with that asset. The valuation method for trademark and brand is commonly used royalty method, which is the present value of the royalties avoided for use of the asset. I’m going to give you the case for excess earnings, which is called multi-period excess earnings (MPEM) for customer relationship valuation, which is the net incremental cash flows that the relationships generate net of the contribution of supporting assets. Both methods involve making assumptions about future performance, discount rates, tax rates, and asset usable lives. The intangible assets are recognized and measured at acquisition date and then amortized over the useful lives of such assets (usually 3 to 20 years, depending on the type of asset) and subject to annual review for impairment in accordance with IAS 38. Leaves long-term consequences in the financial statements for the allocation decision of the initial IFRS 3 PPA valuation services.

What Are the Best Practices and Processes for IFRS 3 Compliance?

The purchase price allocation process must be structured and disciplined in order to be successful, based on IFRS 3. There are usually five stages in the process. First, get a timeframe of the transaction and team alignment – involve valuation experts early, define documentation process, define roles and responsibilities. Secondly, take a detailed asset and liability review, review contracts, look at the intellectual property registers, review customer data, review technology documentation, etc. and decide which assets meet the IFRS 3 recognition criteria for assets. Third, collect financial and operational information – historical financial statements, customer retention statistics, margin statistics, revenue projections, competitive information, industry data and statistics needed to value models. Fourth, choose and implement proper valuation techniques for each category of asset: calibrate assumptions to available market data and comparable transactions. Fifth, record every decision, assumption and calculation in a thorough valuation report that can be audited and attacked by tax authorities. Other best practices include: hiring independent valuers with IFRS 3 experience to ensure independent valuation; getting audit committee pre-approval of the valuation method and assumptions; keeping robust workpapers that will allow for review of all assumptions; conducting careful controls to ensure data accuracy and model integrity; dedicating time to sensitivity analysis to understand which assumptions have the most material impact on the allocation.

The lessons learnt from experience in real world of acquisition accounting reiterate the key success factors. Companies that allocate the purchase price properly and defensibly generally invest heavily in data collection during the due diligence process and set up baseline financial and operating metrics prior to closing. They involve valuation professionals in deal structuring, rather than after closing, to discuss and agree on allocation methodology, and to avoid retroactive allocation decisions. They have good records documenting the allocation of the purchase price, assets recognized, method of accounting, and any assumptions made. Also, they are flexible – if the assumptions turn out to be materially wrong during the measurement period, they change the assumptions, stating the reason for the change. Last but not least, they don’t see IFRS 3 PPA valuation services as a compliance-related measure, but rather as a strategic tool when making decisions after the acquisition and tracking synergies. Knowing what assets contributed to the price paid for the acquisition will help management determine if the synergies they targeted are being achieved, and if the investment case is still viable.

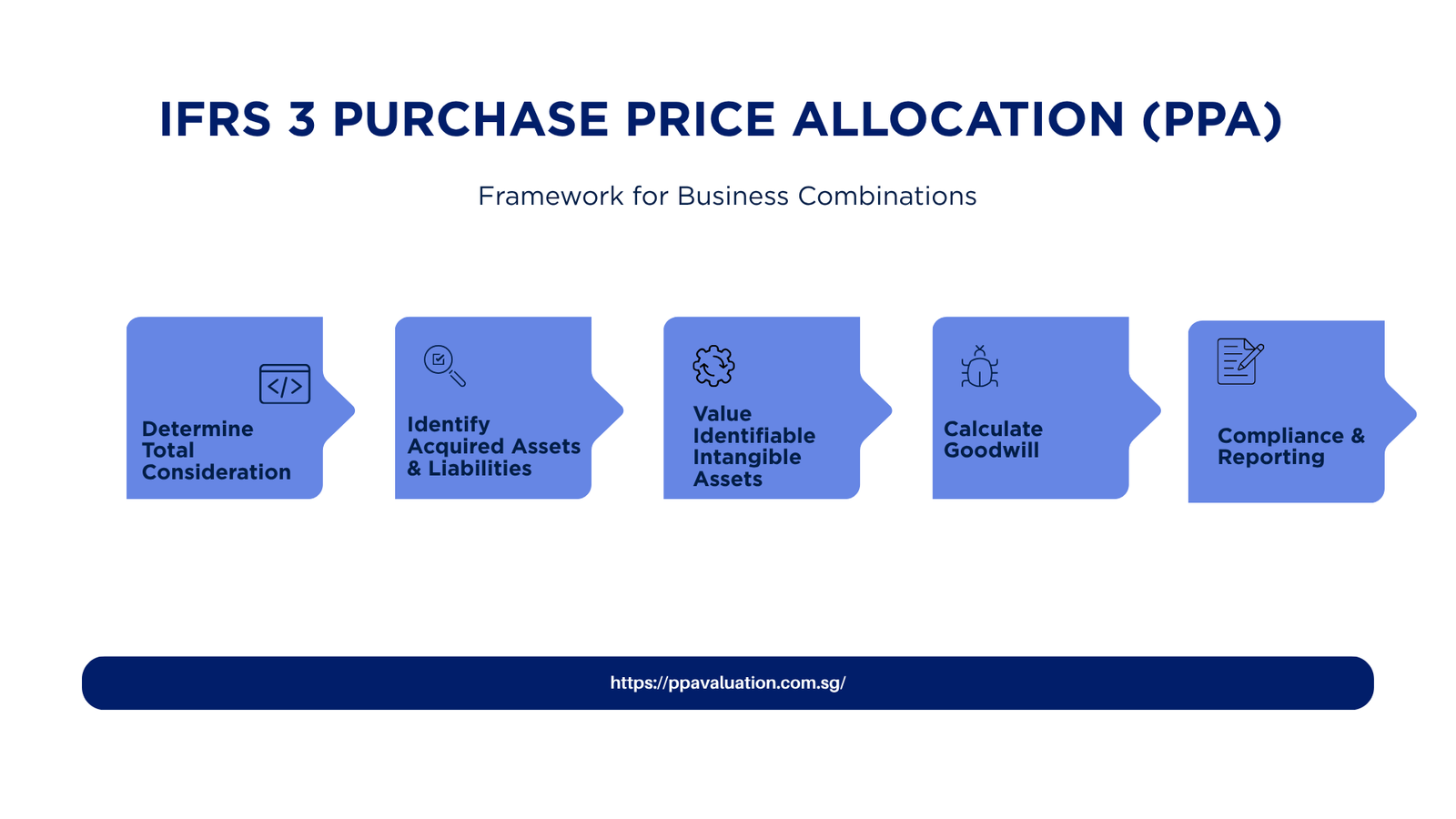

Five Key Steps for Implementing Purchase Price Allocation Under IFRS 3

- Determine the date of the acquisition and the total consideration transferred: Record all of the consideration transferred (cash, equity, debt, contingent consideration) at fair value to calculate the total acquisition price.

- Carry out an in-depth asset and liability audit: Review the target’s contracts, IP registers, customer information and operating processes to determine what assets and liabilities can be considered for recognition; determine whether items are in accordance with IFRS 3 recognition criteria.

- Collect and choose valuation techniques: Prepare historical financial statements, customer data, competitive information, and industry data; select valuation approaches based on historical financial statements, customer information, competitive information, and industry information that are appropriate for each asset category and in line with market practice.

- Apply valuation models with key assumptions, determine value allocations with best-estimate assumptions, recognize goodwill as a residual of the consideration, test sensitivity of key assumptions for understanding driver and risk.

- Document and validate: Prepare and document valuation reports with clear methodology and supporting assumptions/claims for management sign off; seek auditor validation of approach and compliance with tax and regulatory requirements; keep records for tax and regulatory review.

Real-World Examples and Case Studies

Let’s say a global food and drink company buys a local beauty brand for $500 million. The target’s balance sheet indicates that it has tangible net assets of $80 million, mainly in the form of inventory and equipment. The remaining $420 million has to be spent on intangible assets and goodwill. Experts in IFRS valuation of intangible assets determined the value of the brand trademark at $150 million (based on relief from royalty), the value of customer relationships at $120 million (based on MPEM in accordance with the repeat purchase rate), the value of proprietary formulations and technologies at $70 million, and the value of advantageous supply contracts at $40 million. This is a better allocation of the excess than just the accounting goodwill approach that leaves only $40 million in goodwill. There are also material tax benefits with the allocation, with the $150 million in brand allocation creating a 10-year tax deduction (if allowed under the tax laws) for $15 million annual tax deductions and a big cash flow benefit. This is like the second scenario, a software firm buying another smaller firm for $100 million when it only had tangible assets of $20 million. The amount for intangible assets of the acquirer is $80 million. Intangibles of value are such as the software platform technology, customer base and staff. The software platform’s value is calculated using the income approach, which yields a value of $35 million based on the incremental licensing revenue that it generates. Based on customer values and retention rates, the value of customer relationships is valued at $28 million. Assembled workforce, typically not separately recognised, is equal to the remaining value of $12 million, recognized only as employees are critical to software support services, a separable contractual element. The value of Goodwill is $5 million. This allocation is not questionable because each of the assets is backed by an observable good metric (software usage, customer churn, staffing costs etc.) and not abstract goodwill.

Benefits and Challenges of Rigorous IFRS 3 PPA

Advantages of detailed purchase price allocation under IFRS 3: There are a number of advantages of detailed purchase price allocation under IFRS 3. Firstly, it offers a tried and tested, and auditable, basis for subsequent financial reporting and tax planning. Second, it helps the management to comprehend what assets were behind the acquisition economics, aiding in the post-acquisition value creation evaluation. Third, it maximizes tax efficiencies through the allocation of purchase price to assets which have beneficial tax attributes (such as customer relationships which can be amortized in many jurisdictions). Fourth, it reduces the chance that future goodwill impairment will occur, because it guarantees that intangible assets are measured fairly, and that goodwill is the remainder of synergistic value. Finally, it aids in strategic decision making by identifying what acquired abilities (technology, brands, customer bases) are most valuable and should be protected or developed.

Challenges: On the other hand, the IFRS 3 intangible asset valuation is complex and expensive. It is time consuming, very expensive and the need for independent valuers, detailed analyses and full documentation is required. Unnecessary and undue judgmental assumptions regarding discount rates, growth rates and asset useful lives can cause audit disagreements and tax issues. Valuation assumptions are subject to reexamination in the face of volatile market conditions in the measurement period. Impairment testing and useful-life reviews of recognized intangible assets create an ongoing compliance burden. Furthermore, the recognition and amortization of large values of intangible assets can cause a significant reduction in reported earnings in the years after acquisition, which could underreport the earnings needed to meet the expectations of investors for acquisition accretion. Rigorous and practical are thus necessary.

Frequently Asked Questions (FAQ)

- What is the difference between purchase price allocation and goodwill impairment?

Purchase price allocation under IFRS 3 is only done once – at the date of acquisition – to measure all acquired assets and liabilities fairly and to calculate the initial goodwill. According to IAS 36, goodwill impairment is carried out every year after that and involves determining whether the goodwill is recoverable (or not). When the acquisition fails to perform well, goodwill is diminished. If the value of intangible assets with finite lives are undervalued, then the amortization expense will be less and earnings will be overstated. The following effects are separate from the initial allocation and are postacquisition.

- Can purchase price allocation be changed after the measurement period?

IFRS 3 allows for any adjustment to the allocation during the measurement period (up to 12 months from the acquisition date) only if there is new information regarding facts and circumstances that existed at the acquisition date. This is referred to as a measurement period adjustment. Changes after the measurement period are not allowed unless the changes are due to changes in contingent consideration. This finality is crucial for the stability of financial reporting, but also makes it a rush to perform IFRS 3 PPA valuation services in a timely and accurate manner before the deadline.

- How are contingent payments treated in purchase price allocation?

Contingent consideration (such as an earnout based on postacquisition performance) is valued at fair value at the acquisition date and added to the total consideration. The adjustment is posted to the income statement, not as a measurement period adjustment, if the contingent payment ultimately turns out to be different than the original estimate of the cost due to changes in estimates or circumstances. This may be a cause for fluctuations in earnings if earnout targets are not achieved.

- What happens if an acquired intangible asset is overvalued?

IFRS 3 intangible asset valuation will be overly optimistic in two respects. First, amortization expense will be overstated, thus lowering net earnings over the life of the asset. Secondly, if the asset is subsequently impaired (for instance, when the number of customers leaves the business at a higher rate than anticipated or when technology changes out quicker than anticipated), the impairment charge is added to the profit or loss statement. Both of these will impact equity and earnings, which may result in disappointment to the investors and failure to comply with the covenants or ratios.

- How do tax authorities challenge purchase price allocation?

The transfer pricing principles are also considered in the review of IFRS 3 PPA valuation services by tax authorities to ensure that the allocation of income is appropriate. They may contest allocations made to intangible assets that have little to no tax basis and high book value or allocations that delay taxable gains. Keeping up-to-date records and following reasonable methods in line with the market’s practice is the best protection.

- What valuation methods are most defensible for customer relationships?

The multi-period excess earnings method (MPEM) is the most popular and sound method of valuation for customer relations. The net incremental cash flows from customer relationships, net of the contributory value of supporting assets (such as workforce, technology). It accounts for the observed customer behaviour data, retention and margin profiles and brings in a reality check of the company-based metrics rather than the abstraction of multiples.

- How often are intangible asset useful lives reassessed after acquisition?

There is a review by the company accounting every year, useful lives are re-evaluated. When facts change significantly, such as a customer relationship asset is discovered to have a shorter useful life than previously thought, or technology is found to be outmoded quicker than anticipated, the remaining amortization is adjusted prospectively and the useful life is shortened. These changes are revealed in the notes to the financial statements. The IFRS 3 intangible asset valuation decisions consequently result in long-term accounting requirements that are much longer than the measurement period. measurement period.

Conclusion: Actionable Insights for Finance Professionals

Doing the purchase price allocation under IFRS 3 is more than a compliance activity – it is an essential building block for the future success of the business. Defensible IFRS 3 PPA valuations provide rigorous and defensible valuation services, which give the organization an understanding of what is truly being acquired, maximizing tax implications, reducing future impairment risk and aiding in decision making. Purchase price allocation should be a disciplined and rigorous process that involves qualified valuation professionals, the collection of complete data, the use of a process consistent with market practice, and the complete documentation of the process. Taking time to carefully analyze PPAs during the measurement period reaps benefits over time: It reduces audit risk, bolsters defensible tax positions and provides a better understanding of whether acquired assets are creating value. Understanding IFRS 3 intangible asset valuation is a good stepping stone for a career change for junior to mid-level level professionals coming into the acquisition world. The organizations that are the best at allocating purchase prices have established a process: they have clear protocols, they have very skilled teams that execute the process, they have independent validation of the process and they have learned and improved from previous transactions. Despite trading and acquisitions, IFRS 3 PPA valuation services will continue to play a vital role in ensuring the integrity of financial reporting and value creation. Developing these skills and systems early on equips professionals to make a positive impact in their organizations’ deal success.